EXECUTIVE SUMMARY

- On January 7, 2025, the Consumer Financial Protection Bureau issued a final rule to amend Regulation V, which implements the Fair Credit Reporting Act.

- The new regulation intends to prevent creditors, rating agencies, and health care providers from accessing medical debt information.

- Hiding medical debt will increase credit risk, and force health care providers to more frequently require up-front payments, leading to an increase in high-risk borrowing and worse health care outcomes.

INTRODUCTION

Effective on March 17, 2025, the Consumer Financial Protection Bureau (CFPB) will amend Regulation V, which implements provisions from the Fair Credit Reporting Act (FCRA). This rule will place a “restriction on sharing of medical information,” between patients, health care providers, and credit stakeholders. In essence, this rule will prevent the sharing of medical debt information with entities that assess and determine credit risk, and more crucially, with lenders that create payment plans for people receiving health care services.

According to the CFPB’s notice on the rule, this decision was largely guided by “recognizing the uniquely sensitive nature” of medical history, in addition to an agency obligation to implement FCRA statutory provisions. The CFPB claims that this revision of Regulation V will remove $49 billion in medical debt from 15 million Americans’ credit reports, increasing FICO scores by an average of 20 points.

While the CFPB and the politicians in support of this rule see this change as a necessary step in providing welfare and privacy to millions of Americans, a policy that functionally hides medical debt will have unintended consequences. Creditors and health care providers may limit access to services, leading to more costly borrowing alternatives, and worse health care outcomes.

REGULATION V AMENDMENT

In simple terms, Regulation V (12 CFR Part 1022) is designed to prevent certain private information about a debtor’s history from being used to determine credit eligibility. The FCRA included this regulation primarily for the purpose of protecting consumers from identity theft and affiliate marketing. With the newly amended Subpart D, on Medical Information, the scope of Regulation V has expanded to include all medical bills.

In short, the new rule removes a “financial information exception” from a 2005 regulation. The CFPB stated that revoking the 2005 rule will ensure “…creditor[s] will no longer be able to consider medical information…” when determining a “…consumer’s eligibility, or continued eligibility, for credit…” To paraphrase, creditors will be denied full transparency about consumers’ medical debt history, and by extension, their ability to make payments on loans.

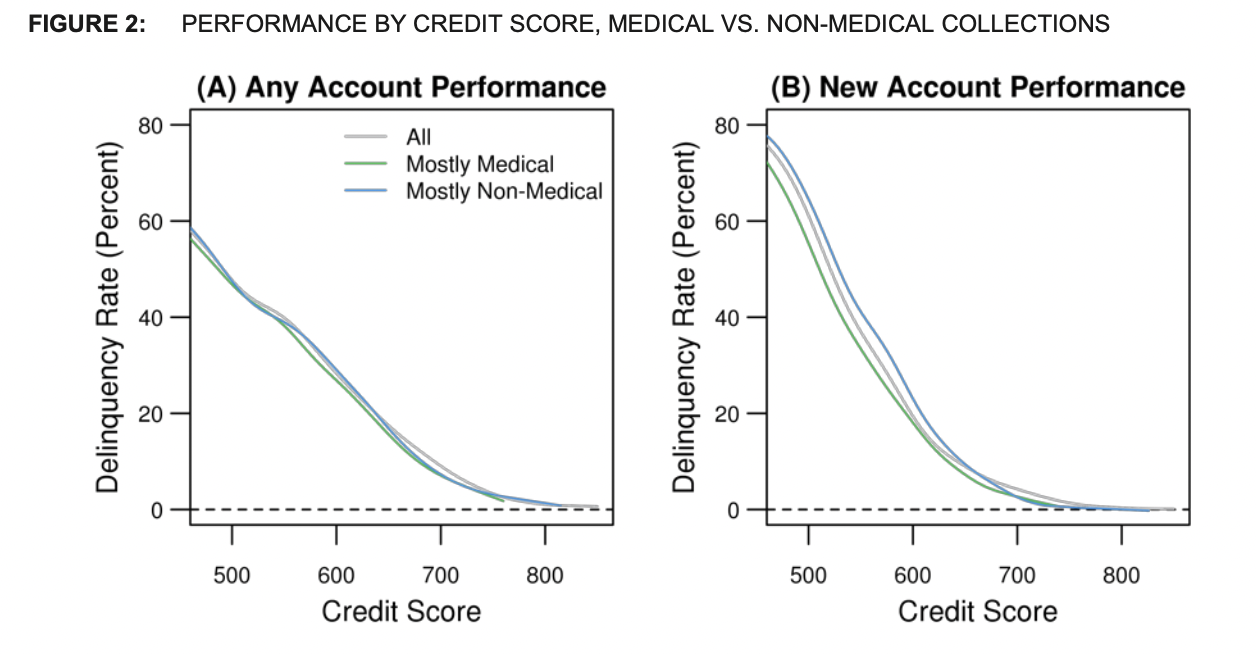

The CFPB, under the leadership of former agency Director Rohit Chopra, cited research that shows “…medical debt has limited predictive value in predicting future default…[and] may be less predictive of whether a consumer will pay a future loan…,” which helped inform the agency’s new rule. A study from the Consumer Financial Protection Bureau’s Office of Research from 2014 showed that delinquency rates for individuals with ‘mostly medical collections’ were only marginally lower than individuals with ‘mostly non-medical collections’ with the same credit score; suggesting, the two groups are “not equally predictive of delinquency.”

Source: https://files.consumerfinance.gov/f/201405_cfpb_report_data-point_medical-debt-credit-scores.pdf

FAULTY LOGIC OF HIDING MEDICAL DEBT

First and foremost, hiding medical debt does not make the debt go away. The amendment of Regulation V does not prevent debt collection agencies from pursuing unpaid amounts when adequate legal substantiation is obtained. Health care providers, and private hospitals in particular, typically operate at a 2-3 percent Bad Debt Percentage benchmark – meaning the creditors only write off a small number of missing payments. Cash flow is an essential aspect of maintaining any business and health care providers will continue to not overlook this even at the expense of their patients’ financial security.

Secondly, because money is fungible, the amount of medical debt will always ultimately be decided by debtors. When an individual incurs debt on multiple loans, there is no set determination on which balance is prioritized by the debtor. Assuming all consumers make rational decisions, the debtor will choose to pay the debt that will most likely result in collections and/or a substantial decrease in credit score. Naturally, when a law is put in place that protects people with medical debt from having that information shared with credit stakeholders, those bills will be the last to be paid. When given the choice to default on a loan that cannot be reported to rating agencies, or to default on a loan that will be reported, consumers will always choose the former.

Lastly, it is important to remember that credit score is not a measure of whether an individual is deserving of a service, but rather a calculated measure of their ability to afford the service. When delinquencies are overlooked in one area and credit scores are artificially protected, creditors will have a more difficult process in determining fair and effective payment plans for their clients.

IMPLICATIONS IN HEALTH CARE & THE CREDIT MARKET

While it is difficult to definitively quantify the net impact of hiding medical debt on credit markets and the health care sector, many experts are justifiably wary. As previously mentioned, the amendment to Regulation V does not address the root cause of defaults and instead attempts to hide poor performance at the expense of favorable lending conditions. Both creditors and service providers will undoubtedly shift practices to adjust for these changes, causing further problems. The extent of stakeholder retaliation has yet to be seen, but projections suggest that health care providers will demand more payment up front; and consequently, those most vulnerable will resort to predatory loans.

Much like any other business, health care providers will adjust payment models to maximize profits. Making sense of the new Regulation V – and its effects on their ability to make collections – health care providers may attempt to counteract increased default risk by demanding higher payments upfront. This may not be such a big deal for menial low-cost treatments – as the default risk is already low – but could have ramifications for more serious high-cost procedures. In instances when health care providers are not required to give emergency care, they reserve the right to refuse treatment until payment in full. Of course, if this trend were to grow, the United States could expect to see denial of quality access to care for millions of low-income Americans.

With access to health care services being limited by new payment models, consumers will turn to high-risk borrowing structures. This problem may be exacerbated by a general decrease in the supply of mainstream credit caused by the new regulations enforced on debt collection agencies. According to one study, this reduced access to credit will lead to a corresponding increase in payday loans. This would be a devastating outcome for consumers, as typical two-week payday loans with $15 fees per $100 borrowed come with an annual interest rate of 400 percent; more than 200 percent higher than average subprime loans. These alternative lines of credit for individuals needing health care services would no doubt be more costly than the previous model and point to an oversight in the intended goals of the CFPB’s new amendment.

NEW DEVELOPMENTS

With the Trump Administration coming into office last month, the CFPB’s rule is subject to further review. The White House announced their broad 10-to-1 Deregulation Initiative, which promises a tenfold decrease in rules and regulations issued by all federal agencies. This initiative is concurrent with the President’s executive order to freeze all pending agency rules for 60 days. These developments will complicate and stall the CFPB’s rulemaking process but have yet to definitively stop the medical debt rule.

CONCLUSION

The Consumer Financial Protection Bureau’s implementation of the new rule amending Regulation V functionally hides medical debt from credit stakeholders and healthcare providers. Removing medical debt from credit reports will increase credit risk, leading stakeholders to alter business practices. These changes will limit access to mainstream lines of credit and quality health care, leading to worse outcomes for millions of Americans.

You must be logged in to post a comment.