On March 29, 2013 the Southern District Court of New York issued a judicial decision that fundamentally altered the foundations of the world economy – and no one noticed. The case in question was an anti-trust suit brought against Bank of America as a part of the ongoing fallout from the Libor manipulation scandal, but the decision has implications that reach far beyond the Libor scandal itself.

Libor Nightmare:

The London Interbank Offered Rate, or Libor, is supposed to represent an honest estimation of the interest rates banks would offer each other for loans. That probably sounds fairly innocuous, but the Libor rate has come to dictate interest rates for over $350 trillion (yes, trillion with a ‘t’) in investments.

Sometime in 2005, British mega-bank Barclays discovered that if they simply made up the estimates – as opposed to reporting honest predictions – of interest rates, they could swing the Libor in whatever direction would make them the most money on a given day. Shortly thereafter, all the other big players jumped into the game: Bank of America, JP Morgan Chase, Citibank, Credit Suisse, Deutsche Bank, HSBC, Lloyds of London, RBS, UBS, and at least ten others.

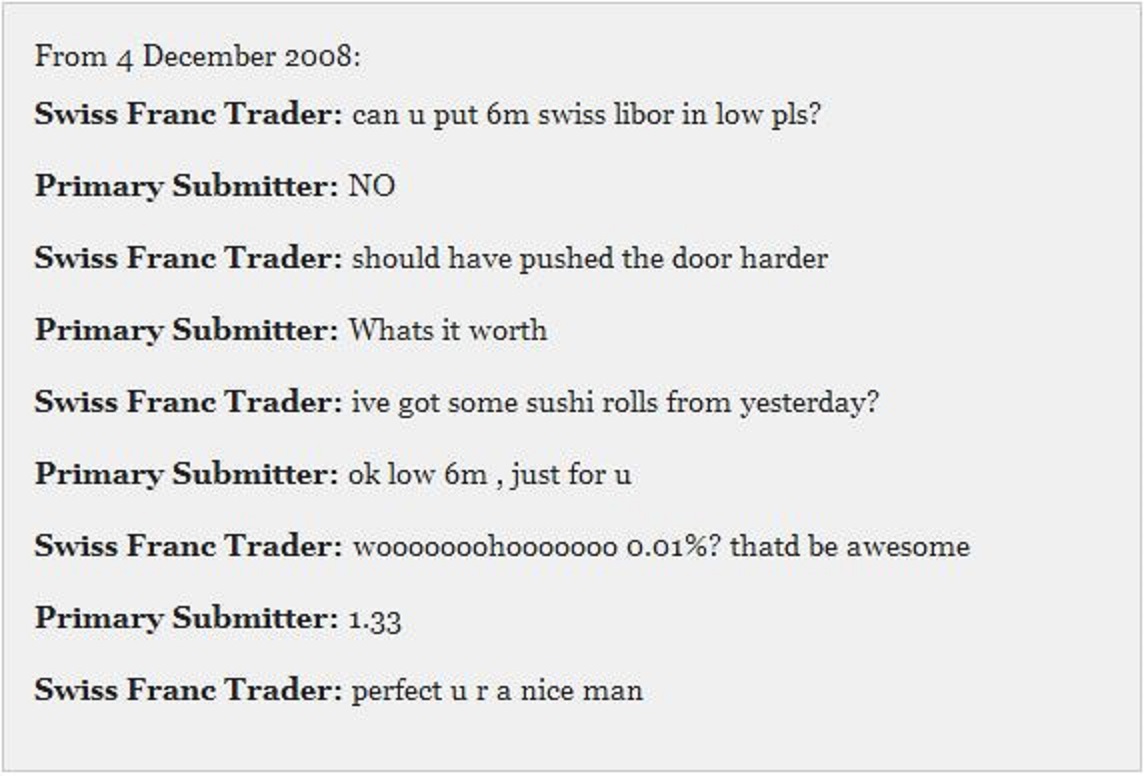

The above conversation, one of dozens of similar communications, is representative of the blatant manipulation banks were involved in, and in case you missed it, this conversation consisted of a bank employee agreeing to falsify Libor numbers in exchange for day old sushi – one of hundreds of falsifications that resulted in over $10 billion in losses for U.S. cities and towns alone. It is unlikely that we will ever know the full extent of losses to investment funds, pensions, retirement accounts, or individual investors, but they probably total in the tens (if not hundreds) of billions.

The Case:

Predictably, investors were outraged to learn of the collusion affecting their pocketbooks. Lawsuits were quickly filed, most of which are still working their way through the legal system. One of the early decisions, and one that is likely to impact not only the other Libor suits but the financial system as a whole, was recently reached in an anti-trust suit against Bank of America.

Investors claimed that by colluding with other banks to artificially set the Libor rate, Bank of America was engaged in illegal ‘anti-competitive’ behavior. Bank of America responded with a remarkable claim: the Libor rate, long thought to be an indicator of rates on the open market, was in fact not a competitive process. They went on to say that “The plaintiffs, I believe, are confusing a claim of being perhaps deceived with a claim for harm to competition.” Even more remarkable than the argument, was the fact that the judge accepted Bank of America’s assertions and threw out the case.

The Aftermath:

So what does all this mean? Certainly there is quite a bit of forthcoming litigation, and it is not yet clear how the courts will interpret this ruling. However, the ruling could be interpreted as a reversal of previously held beliefs: that major market indicators are based on free market competition.

If the Libor rate was the only instrument of its kind, perhaps this decision would not be terribly problematic. However, this is not the case. Numbers ranging from the ISDAfix rate (a complex financial indicator that underpins another $379 trillion in financial markets) to the price of gold are all set by similar methods – groups of bankers expected to make honest assessments of rates or values.

Speaking of the ISDAfix, it turns out that bankers have being manipulating this rate in exactly the same way. A recent investigation, launched by the US Commodity Futures Trading Commission, alleges that Bank of America, JP Morgan Chase, UBS, and twelve other banks have been colluding and manipulating the ISDAfix rate for their own benefit.

Whatever your views are on financial regulations, this should offend you. When regulations only apply to those who cannot afford the lawyers to fight them, something has gone terribly wrong. We need to either uniformly enforce the regulations we have, or eliminate them. More importantly, we need to make a decision as to whether we intend to allow the banks to continue to set rates for themselves. Every day that the banks are allowed to collude in secret is one more nail in the free market’s coffin.

You must be logged in to post a comment.