In 2013, Kaiser released a poll stating 7 out of 10 young adults rate having health insurance as “very important” and worth spending money on. Yet a recently released Issue Brief on the Marketplace from the Assistant Secretary for Planning and Evaluation (ASPE) shows that in the last three months the “young invincibles” did not purchase health coverage as anticipated. If the average young person does not finding insurance important or worthwhile, what kinds of young adults are singing up? Are they going to be offsetting skyrocketing medical costs as the Affordable Care Act (ACA) planned?

The recently released ASPE Issue Brief from the Department of Health and Human Services summarizes the Marketplace activity between October 1, 2013 and December 28, 2013. The report highlights several aspects of the implementation process such as enrollment figures based on gender, age, metal level, and federal assistance. According to the report, “24 percent of the persons who have selected a Marketplace plan are between the ages of 18 and 34”. The cumulative Marketplace enrollment over the three-month span totaled at 2,153,421 indicating less than 520,000 of those enrollments fall into the 18-34 age range. This is a far cry from the 2.7 million enrollees the Obama Administration estimated necessary for implementation success.

The issue brief left policy wonks everywhere wanting more information about the purchasing details of the “young invincibles”. Are those 520,000 young people purchasing bare bones catastrophic and bronze plans or spending extra for silver, gold and platinum plans. Furthermore, can we use an individual’s metal level choice as an indication of their health and medical needs?

While knowing what plans these individuals purchased would not provide us an accurate assessment of their health or anticipated medical expenses, it would raise concerns if large numbers of young adults are purchasing anything above the bronze plan.

The United States’ young adults have been slated as the cornerstone of the ACA, mandated to pay into a system in which the average young person will receive considerable less services compared to older generations more prone to illness. Their participation is necessary to maintain the “affordable” premium levels for all. As older generations and some of the sickest individuals are reintroduced into the market and require large amounts of medical attention, the higher cost of coverage associated with this group must be offset by young, healthy individuals paying into premiums and not seeking medical care.

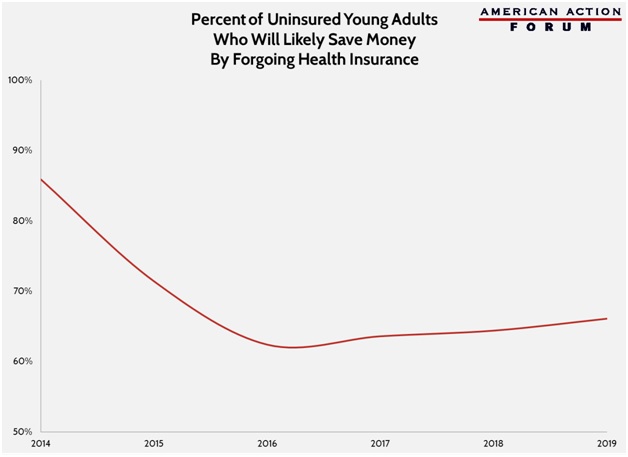

Participation was supposed to be generated through general individual interest and avoidance of annual penalty fees for the uninsured. However, individuals don’t seem to be showing interest and penalty payments are not anticipated to dramatically impact enrollment numbers. The ACA was designed to gradually increase in penalty fines for individuals who do not get coverage. During 2014, any individual who does not have appropriate coverage will be charged 1% of the yearly household income or $95, 2% or $325 in 2015 and 2.5% or $695 each year following plus inflation. According to recent research from the American Action Forum, “6 out of 7 uninsured, young adult households will find it financially advantageous to forego health coverage, and instead pay the mandate penalty and cover their own health care costs.” For example, it would be more prudent for an18-34 year old to pay the 1% or $95 penalty over the monthly premiums averaging in 2014 at $328 for a silver plan. See the below graph from the American Action Forum for more details.

As of yet, enrollment numbers have not supported the claim that young adults purchase health insurance based on personal importance or to avoid current penalty rates. As a result, how healthy can we assume these 520,000 18-34 year olds are who find it important and necessary? The young and invincible are not without illness. An increasing prevalence of obesity, diabetes and other chronic conditions in our society impacts all generations, including our youth. These young adults will require medical attention and accrue high medical costs just as any individual with a chronic disease. These individuals may be anticipating large medical costs and thus, purchasing silver, gold and platinum plans as a result. In this scenario, the budget neutralizers would actually be adding to the costly system, at least until the additional 2.18 million “young invincibles” find their own motivation to pay into a system without much promise of using it. While the economic outcome of this legislation has yet to be established, getting a more clear understanding of our purchasing “young invincibles” would be a step forward in creating better, more successful and economically sound legislation.

You must be logged in to post a comment.