Why we should Still Worry about the Deficit

On October 15, the Department of The Treasury released the final budget results from Fiscal Year (FY) 2014. The results showed an overall deficit of $483 billion, $197 billion less than in 2013 ($680 billion), which amounts to a reduction of the deficit as a percentage of GDP from 4.1 to 2.8. While the Obama administration would like to celebrate this as a noble achievement of fiscal stewardship, a thorough look at the forces influencing the deficit tells a different story. In fact, the underlying forces of the improving economy have played a far greater role in reducing the deficit than any specific policies have. While some would say we no longer need to worry about the deficit, as you will see, the underlying forces tell us that much of the improvements are not due to changes in policy.

Public discourse on deficits is principally concerned with headline deficits, the current mismatch between government spending and tax revenues. While informative, headline deficits are also influenced by a series of factors not affected by the current administration, such as the business cycle. During recessions, federal tax revenues decline automatically with the reduction in output and income. Similarly, certain expenditures such as unemployment insurance automatically increase. In assessing budget deficits, one ought to take these cyclical effects into consideration. In theory, one might otherwise conclude that the deficit is “under control” when the overall deficit is small due to a booming economy, or “out of control” when the overall deficit is large due to a severe recession when the difference could be caused solely by the business cycle.

Automatic Stabilizers

The first step to get a better representation of the deficit is to adjust for automatic stabilizers (AS). The Congressional Budget Office (CBO) uses statistical techniques to estimate the automatic effects of the business cycle on federal revenues and outlays and thus federal budget deficits. The CBO calls this the deficit without automatic stabilizers (sometimes referred to as the structural budget deficit or the cyclically adjusted deficit). This estimation shows that automatic stabilizers have contributed significantly to the deficit since 2007. In 2010, the headline deficit was 2 percentage points higher than it would have been had the recession not set off a series of automatic stabilizers.

Further, when assessing the change in the headline deficit from one year to another, it becomes interesting to note what share of that change was due to automatic stabilizers. An administration could claim to actively be reducing the deficit when deficit reduction is happening due to automatic stabilizers in an improving economy (passively shrinking the deficit). While not the main driver, it is worth noting that of the $197 billion deficit reduction from 2013 to 2014, roughly $18 billion, or about 9 percent, was simply due to automatic stabilizers.

A striking fact when looking at deficits adjusted for automatic stabilizers is how closely it follows the business cycle. If the business cycle had been fully accounted for, one would expect deficits to be uncorrelated with the business cycle. This is in part due to the way the CBO estimates the effects of the business cycle on automatic stabilizers. An important feature of this estimation is that it only accounts for budget changes that are truly automatic, such as unemployment insurance. However, a feature of the real world is that policymakers will frequently, in response to a weak economy, pass legislation that temporarily cuts taxes, increases spending, or both. While such measures are arguably a feature related to the business cycle, they are not automatic, and thus not adjusted for when the CBO adjusts for the cyclicality of automatic stabilizers. The past several years have included a host of legislation that fall into this category including the American Recovery and Reinvestment Act of 2009 (P.L. 111-5) and the Emergency Economic Stabilization Act of 2008 (P.L. 110-343).

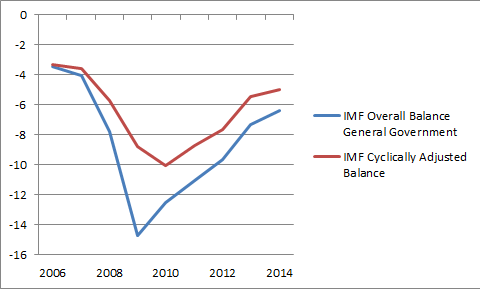

IMF Cyclically Adjusted Budget Balance

The International Monetary Fund (IMF) uses a different technique when estimating their Cyclically Adjusted Budget Balance. In addition to adjusting for cyclical impacts on automatic stabilizers, IMF adjusts for temporary legislative changes and other nonstructural elements (this includes nonstructural elements beyond the economic cycle, which includes temporary financial sectors and asset price movements, as well as one-off, or temporary, revenue or expenditure items). By doing this, the IMF creates a good approximation of the structural balance, the deficit that would have in normal circumstances and which we cannot explain away with the business cycle.

So, how much of the 2013-2014 deficit reduction is due to the expiration of temporary elements? We can’t know the answer until the IMF updates its data set (last updated in April). However, in April the IMF projected that the headline deficit would fall by .9 percentage points in 2014. Of this decrease, .5 percentage points, or 55 percent (!) of the total deficit-reduction, would be due to the general improvement in economic conditions and the expiration of previous temporary legislation. We can thus conclude that while current deficits are coming down, their recent fluctuations have been significantly affected by cyclical components outside the administration’s control. To celebrate this decline as a policy victory would be akin to members of a household attributing change in the weather, from pouring rain to overcast, to its clever weather management strategy.

Thank you for the good writeup. It in fact was a enjoyment account it.

Glance advanced to far delivered agreeable from you!

By the way, how can we communicate?