The Trump Administration has made reforming financial regulation a goal for 2018. Surprisingly, its Democrats that are helping push the effort towards the finish line. Legislation is currently being discussed to roll back Dodd-Frank, a signature bill passed under the Obama Administration that introduced drastic regulations to the banking industry. This bipartisan effort is seeking the first major revision of the 2010 legislation.

In 2017, President Trump ordered Treasury Secretary Steven Mnuchin to review all financial regulations and prepare recommendations designed to improve the safety and efficiency of the industry. The Treasury recommended several actions for financial regulatory reform. These included restructuring the CFPB, reforming the Volcker Rule, particularly for firms with less than $10 billion in total assets, conducting stress tests on banks every two years, as opposed to 1, allowing regulators to tailor standards contingent to the size of the bank, modernizing the CRA, and exempting some banks that maintain high levels of capital from regulations.

Some Democrats have decried efforts for reform as dangerous attempts to dismantle regulations that protect consumers and prevent systemic risks in the financial system. But some moderate Democrats have come to the negotiating table, particularly to aid small and mid-size institutions. Even Barney Frank, one of the law’s crafters, has admitted that the law went too far and placed unnecessary burdens on smaller banks.

Rules and Compliance Costs

Let’s first discuss what Dodd-Frank enacted. The legislation was perhaps the most significant reform of the financial industry since the Great Depression.

1) Increased financial oversight of banks, hedge funds and other institutions

2) Gave Federal Reserve power to set higher reserve requirements. This was meant to recapitalize banks, reducing the risks of too big to fail and taxpayer bailouts

3) Introduced the Volcker Rule, which prevents banks from using depositor’s funds to trade on their own account(i.e proprietary trading)

4) Regulates derivatives markets (i.e mortgage backed securities)

5) Established more oversight of credit rating agencies

6) Establish the Consumer Financial Protection Bureau, an agency that oversees consumer loans and regulates lending

The crisis exposed the banking industry’s equity reserves as dangerously thin. The six largest bank-holding companies in the US had capital reserves of less than 8% in 2007. Improvements in capital requirements have made banks more equipped for future economic downturns. Further, allowing the Federal Reserve to conduct stress tests helps determine whether a bank has enough capital to survive a recession. The financial system also needed increased safety and transparency in derivatives markets. Dodd Frank has helped make the system more secure and reduced systemic risk. However, the legislation has resulted in various unintended consequences and excessive complication.

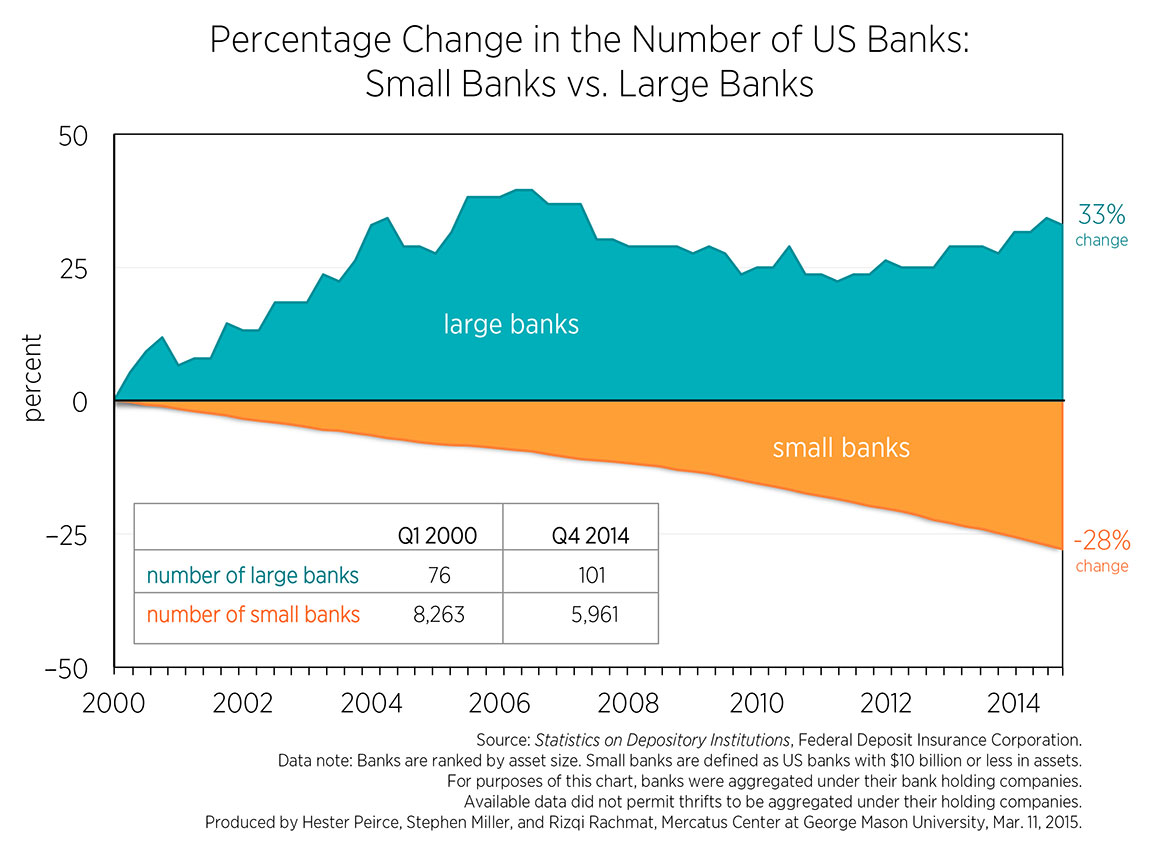

First, the law has levied burdensome regulations on so-called “community banks”. These are small and mid-sized financial institutions that hold less than $10 billion in total assets. According to The Economist, of the near 5,000 US commercial banks, all but around 100 hold $10 billion or less in assets. Some 5,000 banks even hold assets of less than $1 billion. Dodd-Frank has labelled these institutions “systemically important” and thus subjects them to strong oversight. However, most of these institutions didn’t significantly contribute to the financial crisis.

Community banks already face competitive disadvantages. They lack scale, their risks are locally concentrated, thus lacking diversification, and they face competition from large banks and online lenders that offer cheaper alternatives.

Compliance costs are largely to blame for hindering small banks. A study by the Mercatus Center found that compliance costs had risen for 90% of all banks surveyed(nearly 200 banks with assets less than $10 billion). It is estimated that Dodd-Frank has resulted in 27,000 new rules since its inception. A study by the Minneapolis Federal Reserve found that adding two extra members to compliance departments puts 1/3 of small banks into the red.

These excessive compliance costs have also likely contributed to the continuing decline in small sized institutions. For example, Dodd-Frank has complicated the mortgage market, making it difficult and costly for banks to lend. As a result, many small banks have eliminated certain services, particularly related to residential mortgages, mortgage servicing and home equity lines of credit. A Mercatus Center study attributes this to mortgage lending restrictions. While some institutions will cease these services, others plan to engage in mergers and acquisitions in the near term, leading to consolidation and thus, less small firms. An FDIC chart shows that small banks have been in decline since the early 2000s.

How to Reform

Community banks offer a source of financing for small and local businesses, consisting of more than 1/3 of small business loans. Reform should be centered around offering regulatory relief for smaller institutions and creating a better lending environment.

One way to improve the system is to raise the asset threshold for labelling banks as a “systematic threat”. $50 billion in assets essentially designates a bank as “Too Big Too Fail”, subjecting them to detailed stress tests. The asset level is too low and unfairly targets smaller firms.

Community banks are also subject to the Volcker Rule. This controversial provision bans banks from trading securities for their own profit using deposits, an act known as proprietary trading. This hurts liquidity and wasn’t very relevant in the crisis. It simply results in excess compliance costs. The provision is also incredibly vague and at the mercy of interpretation. Institutions with less than $10 billion should be exempt.

The Trump Administration should also consider implications of international banking standards. Basel 3, which states the international capital and leverage requirements to maintain a sufficient level of liquidity, also inhibits small firms.

Senate Bipartisan bill

The bill being debated in the Senate known as The Economic Growth, Regulatory Relief and Consumer Protection Act focuses on small bank de-regulation. It would lift the asset threshold at which a bank is considered systematically important from $50 billion to $250 billion, applying to roughly 10 banks and reducing the effects of too big to fail. Banks with assets of $50-$100 billion would be immediately relieved of regulation and be exempt from stress tests. And banks with $100-$200 billion would lose many of the Dodd-Frank regulations after 18 months. However, institutions with $100-$200 billion could still be subject to Federal Reserve stress tests. Banks with less than $10 billion would be relieved of the Volcker Rule, in addition to receiving capital requirement relief and less mortgage lending restrictions. Most lending firms have less than $10 billion.

What the bill lacks

The proposal is more specifically tailored and lacks broader reforms. The Community Reinvestment Act, which seeks to prevent redlining, should be modernized. It must be more flexible to allow banks to use more resources to meet the needs of low income communities.

The CFPB should also be restructured. The agency is currently funded by the Fed. It should be funded by Congress. Further, the leadership structure at the Bureau has 1 director, unlike other agencies that are led by commissions. An expansion of the leadership team will promote a more diverse and bipartisan agency. The director’s role should also be more defined and limited, giving regulators less discretion to interpret laws.

Conclusion

While these reforms are absent from the bill, the proposed legislation should be a welcome sign. And it has garnered the support of some eleven moderate Senate Democrats, including Heidi Heitkamp and Mark Warner. This is very important as it allows the Senate to overcome a possible Democratic filibuster. Senate Majority leader McConnel has stated that “I think we have a good chance of passing that(the bill) and it would have to be done on a bipartisan basis”.

The new central banking environment also seems welcoming to reform. The recently appointed Federal Reserve Chairman, Jay Powell, has implied he is open to reducing regulations, something his predecessor Janet Yellen didn’t entertain. Though he has stated capital requirements should remain strong, Powell has implied that requirements such as the Volcker Rule on community banks should be relaxed.

The goal should be to reduce red tape, while also holding the industry to high capital standards. Stress tests for systemically important firms should be maintained to keep an eye on capital levels. The crisis showed that banks had too little reserves to absorb losses, but excessive regulations have helped form a barrier of entry for small banks that lack the resources to handle compliance costs. It has been nine years since Congress has reformed the financial regulatory environment. It should not botch this bipartisan opportunity.

{kind=link}