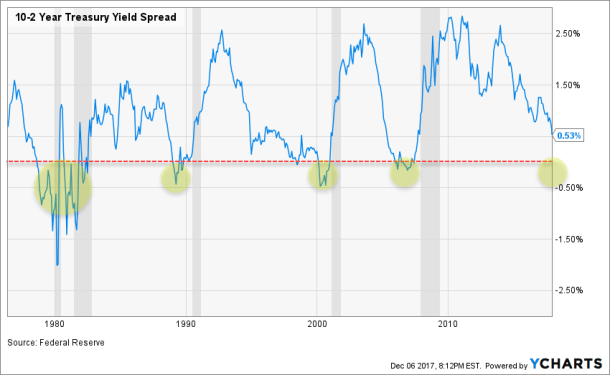

One of the most reliable recession indicators is the yield curve, which measures the spread between short and long duration bond yields. A steeper curve, or when long term yields exceed short term yields, is usually associated with higher inflation and economic expansion. Contracting yield spreads, in contrast, usually suggests slower growth and tighter monetary policy. Short-term treasuries pay lower yields in compensation for purchasing a more risk-averse asset. When longer duration yields, including the 10-year note, fall below short-term ones, such as the 2-year treasury, the yield curve inverts. As shown in the chart below, an inversion of the curve, has preceded the past five economic downturns, including in 2007 and 2001.

Yield Curve Significance

Not too long ago, many worried that the 10-year treasury yield, which was hovering around 2.9%, would break out above 3%. Yields shot up to 2.94 on Feb 21, a four year high, after data emerged showing strong economic conditions and higher wages. This prompted anticipation that the Fed would have to hike rates four times in 2018 to put a lid on inflation.

The gap between short and long-term treasury yields has since narrowed and thus flattened the curve. The spread between 2s and 10s reached a peak in 2011 at 290 basis points, or 2.9%. On March 27, it was only 53 basis points. The 10-year traded around is 2.75% to end Q1.

Perhaps bond markets got ahead of themselves in assuming economic data would call for more rate hikes. Inflation concerns have receded as wage pressures and job market data have not indicated sustainable increases in labor costs.

The decline in the 10-year yield likely resulted from investors fleeing to safe assets in reaction to a spike in equity volatility. Demand for government debt pushes bond prices upward, thus bringing yields down. Concerns of inflation have also subsided, making bonds look more attractive.

The two-year yield, moving in the opposite direction, recently climbed to 2.27%, its highest point since 2008. This largely is in reaction to the Fed signaling it will continue raising short term rates in 2018, while expediting that process in 2019 and 2020. Since the Fed controls short-term rates, 2-year note yields are more correlated to Fed rate hikes.

Economic Cycle

In this late stage of the economic cycle, the Federal Reserve usually begins to raise the federal funds rate to combat inflation. Short term rates usually rise in tandem. However, unique to this 10-year bull market, we have yet to see inflation rise above 2%, which has helped prevent longer term yields from breaking out above 3%.

The Federal Reserve has kept an eye on treasury markets. Fed Chair, Jerome Powell, when asked about whether an inverted yield curve would signal a recession, stated that it may not signal a recession this time. In the past “inflation was allowed to get out of control, and the Fed had to tighten, and put the economy into a recession”. Powell replied, “that’s not really the situation we’re in now”, citing that inflation is still well below the Fed’s 2% target. If economic data weakens, it could put pressure on the Fed to be less ambitious with hiking rates.

However, even if the Fed does enact four hikes this year, current global monetary policy will still put downward pressure on yields. The BOJ and ECB still have very low interest rate policies. This will likely encourage foreign capital to flow into 10-year treasuries, thus keeping yields low and flattening the curve. With the increase in 2-year yields, many believe that the curve will soon invert, foreshadowing a recession.

But does an inverted curve mean a recession is an immediate threat? Not necessarily according to research conducted by LPL Financial. The study, as shown in the figure below, reveals that it took several months for the recession to hit after the curve inverted.

The study would suggest that although the yield curve offers warning signs, it doesn’t serve as an immediate recession indicator. Senior Market Strategist Ryan Detrick stated that “once inverted, it took about 20 more months until a recession started”. Even after the yield curve inverts, recessions usually aren’t too quick to follow. “In other words, the economy is still on quite firm footing, and we see few reasons to expect a recession over the next 12-18 months” Detrick said.

Fundamentals Still Support Higher Long-Term Yields

Global growth is still healthy and projected to continue. The expansionary fiscal policy of the US government this late in the cycle, through tax cuts and increased government spending, will likely prolong economic output, at least in the short term, and push inflation higher, raising long term yields.

Central banks are also in the process of reducing their quantitative easing measures. The Fed has already begun raising rates and reducing its bond purchases. The European Central Bank, Bank of Japan and the Bank of England are in the process of doing the same. With continued growth coupled with the decrease in government debt purchases by central banks, yields should rise.

The New Norm?

An interesting perspective is whether the economy is dealing with adapting to a new normal when it comes to interest rates. The US hasn’t experienced a situation where central banks used an extreme form of bond purchasing to keep rates at or near zero (in some cases negative) on a global scale. Even after five hikes spanning over the past few years, interest rates are still low compared to historical averages. With global central banks continuing to put downward pressure on rates, perhaps the post quantitative-easing world won’t be so accommodative to 4-5% yields on the 10-year.

Yield spreads may continue to narrow, but that may not signal a pending economic downturn. With an unorthodox monetary policy being phased out and government fiscal policy becoming a factor at the tail end of an economic expansion, we face an unprecedented macro environment. One might dare say this time could be different.

And lastly, it’s important to put everything into context. The Fed, in the past, was forced to play catch up with higher prices, hiking rates at an expedited pace and triggering economic downturns. That doesn’t seem to be the case now since inflation is not a current issue. Unless the Fed speeds up the pace of rate hikes, perhaps four times in 2018, 2-year yields likely will slow down.

Conclusion

While there is a gap between an inversion and a recession, a flattening curve could foreshadow a broader recession indicator; depressed loan growth. A steeper curve encourages banks to increase lending activity. Lower yields, however, reduce the profitability of issuing loans. With less capital flowing throughout the economy, growth slows. Loan growth hasn’t been spectacular, but with economic conditions improving, perhaps this will change.

As studies have shown, downturns could be several quarters, even years, into the future after the yield curve inverts. As we haven’t even reached an inverted curve yet, history would suggest that the current economic expansion still has room to run. With the current modest pace of Fed rate hikes perhaps putting a lid on short term treasury yields, we likely won’t see the curve invert for some time.

You must be logged in to post a comment.