Broader choice comes with a price.

As the Affordable Care Act (ACA) slowly phases in, health policy experts predict a primary care physician shortage gap as well as a deep crack in the patient-physician relationship in the United States to grow deeper over time. Especially if the President doesn’t keep the promise he made to the American people no less than 36 times that anyone who liked their present health insurance could keep it.

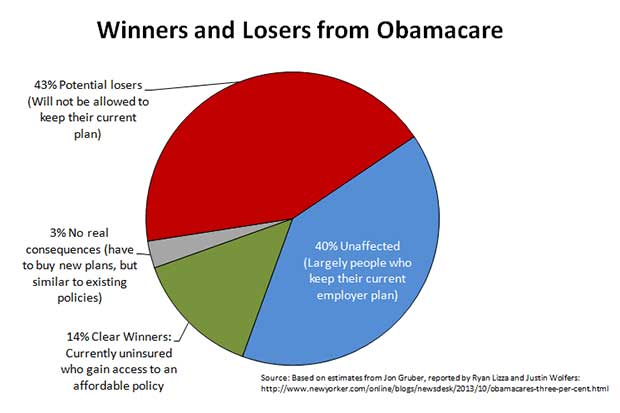

In fact, on November 7, 2013, Fox News reported that more than 4.2 million Americans had received health insurance cancellation notices due to the new regulations. The number of Americans whose individual healthcare plans are cancelled is estimated to be roughly 15.4 million people or approximately five percent of the U.S. population, which truly exceeds the 7 million people the Obama Administration seeks to sign up for Obamacare.

On the other hand, the first period of open enrollment (October 1 – November 2) numbers, publicly released by the Department of Health and Human Services on November 13, in state and federal Marketplaces came to a mere 106,185—a number that shows no mercy compared to the number of those with cancelled plans. Most of which were cancelled because their plans do not comply with Obamacare’s insurance rules and regulations.

Simultaneously, both health insurers and employers are inclined to echo each other in their decision to drop coverage for those Americans left with the shortest sticks of the stack. UPS, Trader Joe’s and Home Depot are no longer providing coverage to some part-time employees. By 2016, the Congressional Budget Office has projected that six million fewer people will receive employer-based health insurance compared with this year.

Stakeholders like the National Retail Federation claim that employers are not only looking for ways to keep their costs under control, but it is suggested that the presence of health exchanges helps to accelerate the trend in dropping coverage for employees. For instance, under the ACA, an individual employee may only receive a tax credit if their employer does not offer insurance through their job’s plan; this condition alone better allows employers to quickly drop coverage for the “benefit of the individual employee.”

Is this the right economic trade-off?

Seems questionable—since those who lose their health insurance are only falling victim to narrow networks in Obama’s health insurance markets.

Matthew Eyles, Vice President of Avalere Health, comments on the issue, “To get to that low premium, the way to get there is by having a more limited or narrow provider network.” The ability to sell less-expensive plans with limited doctors and hospitals helps contain medical inflation, as looser networks could mean higher prices and greater competition. Exchange plans are required to take all applicants, cover broad benefits and provide robust financial protection against catastrophic illness. In return for that, something else has to give. The result: limited choices and significant out-of-pocket costs through deductibles and copayments.

On top of the higher costs to consumers, regulators and elected officials in a several states have already forced damaging changes.

In New York, the Memorial Sloan-Kettering Cancer Center, one of the world’s leading cancer hospitals will not be ‘in network’ for any of the insurance plans on the state’s exchange, leaving approximately 615,000 individuals and 450,000 small business employees with no other option but to seek treatment elsewhere, or pay the bill out-of-pocket.

In Chicago, Rush University Medical Center is now only covered by 38 health plans–down from 71 health plans. A number of the nation’s top hospitals, including the Mayo Clinic in Minnesota; Cedars-Sinai in Los Angeles; and children’s hospitals in Seattle, Houston and St. Louis, are cut out of most plans sold on the exchange.

In Maine, Anthem Blue Cross and Blue Shield proposed to exclude six hospitals in the southern part of the state, yet fortunately state regulators prohibited this change. Excluding certain hospitals from Anthem’s plan, according to a company spokesman, would allow premiums to be twelve percent lower than they otherwise would have been. Once again, the economic trade-off creates winners and losers.

Overall, these narrow networks can force patients to switch doctors, drive long distances for routine or emergency care, and inevitably create more potential problems for patients with any chronic condition or cancer. In fact, this summer Washington Insurance Commissioner Mike Kreidler blocked five insurers from selling through the exchange, which in several cases, would require people to drive nearly fifty miles to see a cardiologist and more than 100 miles to see a gastroenterologist.

Clearly, leaving out specialized care from community networks ensures inadequate access to care and diminishes the value of the patient-physician relationship. Patients’ ability to receive the proper care they need from a provider–whether the provider is a specialist, a primary care physician a patient has seen for years, or a hospital emergency physician–at that moment in time will either be delayed due to a longer commute or an entire change in route. All these relationships will be broken or made close to impossible as long as cost reduction strategies involving narrow networks take precedent over cost reduction strategies to ensure patients with continuous care and widely accessible, affordable health care.

Related articles

- Top Cancer Hospital Not Included on Obamacare Plans Sold in NY (breitbart.com)

You must be logged in to post a comment.