Achieving financial independence has become more difficult for youths in the United States as the length of time necessary to complete education increases and the economy continues to recover from the Great Recession. The typical achievement indicators of adulthood, such as the completion of education and full time employment, as well as the social indicators of marriage and children, are occurring later in life, leaving a group of twenty-somethings in limbo somewhere between youth and adulthood. It has generally been difficult to measure the degree of intrafamilial monetary transfers between parents and children, however, recent studies have attempted to determine whether dependence on parents is increasing.

Jeffrey Jensen Arnett, Ph.D. of Clark University, coined the term “emerging adults” to describe individuals 18 to 29 who are transitioning between school and the workforce, and tend to have some degree of financial dependence on their parents. The University conducted two surveys, the Poll of Emerging Adults and the Poll of Parents of Emerging Adults, in order to acquire data on this transitional generation of Americans.

According to emerging adults surveyed, financial independence has become the second most important factor to achieving adult status, preceded by accepting responsibility for oneself. Forty-four percent of parents say they provide their 18- to 29-year-olds with “frequent support when needed” or “regular support for living expenses” with wealthier parents providing more assistance to their children than lower income parents.

Parents of emerging adults are considered to be part of the sandwich generation; simultaneously planning for retirement while supporting both their parents (directly or through Social Security) and their children. Increased transfers to adult children may alter savings decisions, with money that would otherwise have been used for retirement instead being consumed in the present.

The Population Studies Center of the University of Michigan examined Historical Trends in Parental Financial Support of Young Adults and split the emerging adults group into two sub-groups. Post-adolescents are considered to be individuals 19 to 22 years old while early adults are 23 to 28. The group is divided due to characteristic differences as follows:

| Post Adolescents | Early Adults | |

| Live with parents | 42.3% | 22.8% |

| Student status (full or part-time) | 65.7% | 25.2% |

| Employed full time | 29.1% | 64.7% |

The table above demonstrates the large role that education has in delaying financial independence. The separation between the two groups is also demonstrated in the amount of support received from parents, however, both groups are receiving more support than previous years. For post-adolescents the proportion of students receiving assistance has increased, as well as the amount of assistance they are receiving. For the older cohort, the proportion receiving any support has increased, especially after 2003.

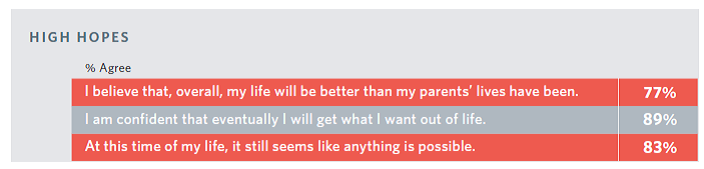

The number of single (unmarried) college graduates is rapidly increasing, however, the proportion of these individuals who are employed fulltime is increasing more slowly. If current education and employment trends continue, the emerging adult demographic is here to stay. With less clearly defined indicators of what it means to be an adult, the implications of a longer transition period, economic or otherwise, are even less clear. However, we’re optimistic. As an emerging/early adult myself, I side with the 83 percent of respondents who believe that “at this time in my life, it still seems like anything is possible” and I’d like to thank my parents for helping me to achieve my goals.

Related articles

- Financial independence ‘key measure of adulthood’ (uswitch.com)

You must be logged in to post a comment.