Aryan Mirchandani

Executive Summary

- The recent AI boom has prompted policymakers to forecast exponential GDP growth in the near term, easing pressure on officials to act against rising national debt levels.

- The Trump Administration has utilized the AI efficiency boom to continue large levels of fiscal spending, as it implores that this boom will decrease our debt-to-GDP ratio, yet the impact that AI will have on near-term economic growth may not be as significant as predicted.

- Debt-to-GDP is the main method investors and policymakers use to view how sustainable a country’s borrowing is relative to the size of its economy; continuity in fiscal policy without GDP expansion could derail the country’s fiscal standing.

Introduction

Historically, only a few technological innovations have created anticipation that rivals the likes of artificial intelligence, which has catapulted the first phase of the new productivity revolution. Proponents of AI argue that it will streamline workflows, enhance decision-making, and unlock rapid efficiencies across wide-ranging industries. The Trump Administration is making bold claims that these gains will help the U.S. balance the debt-to-GDP ratio. Yet, despite rapid diffusion and rising micro-level adoption, the macroeconomic reflection on US GDP data remains ambiguous. When we disentangle the pure efficiency impact of the AI boom from other AI-adjacent GDP factors such as investment, consumption, or labor displacement, illustrated through total factor productivity and labor optimization, we see that AI may not translate into immediate, measurable national output growth.

Background

The relationship between innovation and economic growth is central to macroeconomic theories. If we look at early neoclassical frameworks such as the Solow Growth Model (1956), it treated technological progress as an exogenous factor, something external that could not be explained, which heavily impacts long-term growth. Later scholars, namely Romer (1990) and Aghion and Howitt (1992), looked to formalize the role of technological innovation with endogenous models. They emphasized knowledge growth and human capital accumulation as drivers of growth. Using these models, we can introduce an endogenous variable to represent the productivity gains of AI.

When looking to introduce a variable to represent productivity expansion, research needs to be done into the effect this efficiency can have on the micro level. Empirical evidence of AI efficiency gains remains largely mixed. Brynjolfsson and McAfee (2014) champion AI as a “general-purpose technology” analogous to electricity or the computer. They do this to explain that it will have delayed, but eventually transformative effects on total factor productivity (TFP). Further, we can look to studies from the IMF (2024) and McKinsey (2023) that project automation and algorithmic optimization should lift global GDP by 1-3 percent annually by the 2030s. Yet, skeptics look to Gordon (2016) calls the “productivity paradox,” wherein technological progress at the micro level fails to aggregate into national output gains. This can be for a few reasons, such as slow diffusion across non-digital workstreams, substitution of routine labor without equal or greater output growth, and measurement distortions that underrepresent digital services or efficiency gains.

Holistically, the literature suggests that AI can clearly raise micro-level efficiency, yet its impact on the macroeconomic landscape for GDP depends on the extent to which the gains diffuse across all sectors and get captured by formal productivity metrics. Forward, we will isolate efficiency as the sole channel, agnostic of the AI impact on human capital, investment, and consumption, to illustrate if AI’s impact is transformative or marginal.

Theoretical Framework: Aggregate Production Model

To assess the impact of AI efficiency on GDP, we can adopt Solow’s model on aggregate production.

𝒀=𝑨 ∗ 𝑭(𝑲,𝑳)

Y=Total Output (GDP)

A=Total Factor Productivity (TFP), Technological Innovations

F(K,L)=Labor and Capital

Holding K and L constant (assuming no change in labor quantity, labor hours, or investment into capital), we can see that any rise in total output Y, must arise from an improvement in A, which will represent our productivity growth through AI. Using this structure, AI can function as an accelerator of A, serving to enhance the output creation of both capital and labor without increasing either factor (buying more machines or employing more labor, put simply).

Conceptually, AI can drive efficiency and impact GDP through three key factors.

- Process Optimization: AI automates repetitive and data-intensive tasks, increasing output per labor hour.

- Decision Making: AI can improve resource allocation, supply-chain management, and the utilization of capital.

- Knowledge Expansion: Generative AI and analytical tools can expand the usefulness of human capital by lowering the cost of education for complex tasks.

Yet, these gains are not ensured to translate directly into measured GDP expansion. If these efficiency gains reduce input requirements without raising demand for output, GDP can remain relatively flat or decline nominally. Further, price deflation in digitally enhanced sectors can understate real growth, leading to real misalignment between welfare and GDP. The question, therefore, is not whether AI can increase productivity (it likely does), but whether those efficiency gains are large and diffuse effectively enough to shift GDP growth rates in a meaningful way.

Methodology

To isolate the contribution of AI efficiency to US GDP growth, we can use the Solow residual framework introduced above. We will use three stages to model the impact of isolated efficiency gains. First, we will establish a historical baseline for total factor productivity growth. Second, we will project TFP growth correlated to AI efficiency gains. Third, we will estimate the TFP growth on real GDP growth, holding labor and capital constant.

Efficiency Expansion Model: Historical TFP and GDP Nexus

We can start at the post-2000 U.S. productivity trend to analyze relatively recent data. The Bureau of Labor Statistics (BLS) and the Federal Reserve report that average annual TFP growth from 2000 to 2023 has ranged from 0.4% to 0.6%. This accounts for roughly one-third of real GDP growth during that period.

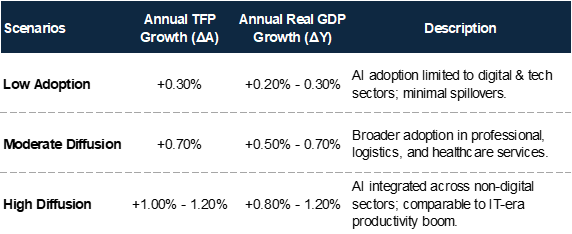

Efficiency Expansion Model: Scenarios

Next, three hypothetical scenarios reflect different levels of diffusion of AI efficiency resulting in various sectors across the economy.

All three scenarios assume that AI only affects growth through efficiency gains, not through increased investment, additional hours worked, or capital growth. This leads us to grab the upper bound of pure productivity and its impact on GDP growth.

Efficiency Expansion Model: Measurement and Limitations

To mitigate real-world complexities, we can adjust using two key factors:

- Diffusion Lag: During the IT revolution, productivity effects took years (often five to ten years) to result in observable TFP growth, highlighting a delay in diffusion and its effect on productivity.

- Mismeasurement Bias: Syverson (2017) and Crouzet & Eberly (2023) argue that digital efficiency reduces costs and enhances quality in ways that are not captured by GDP deflators, which can imply underestimation in true output expansion.

While in the Solow framework, you could reasonably expect a 1:1 correlation between the ∆A and ∆Y, in practice, due to the biases above, we often see a dilution of the change in TFP to real GDP.

Efficiency Expansion Model: Analysis

Low Adoption: In the low adoption scenario, AI-driven efficiency remains concentrated in industries that require high productivity, such as technology and finance. We can see that gains can improve margins and lower costs, but this relates to little true spillover into slower-moving industries such as healthcare or retail, which demand higher diffusion and opportunity sets. This leads GDP to grow marginally, just 0.2% – 0.3%.

Moderate Diffusion: Broader diffusion can lead to stronger growth overall. This would allow AI use cases to impact industries such as logistics, professional services, and manufacturing, which could lift annual growth rates closer to 0.7%. Yet, these are often slower transitions. If we look at historical IT revolution data, it took two decades before digital technology meaningfully impacted national productivity. AI’s success will similarly depend on top-down adaptation, workforce education, and system reconstruction.

High Diffusion: In a high-diffusion case, we can still see a marginally lower impact on real output. This is because much of AI’s efficiency can remain invisible in GDP data. AI often enhances quality rather than quantity; shorter turnarounds, better insights, and improved accuracy can raise welfare and potential output, but do not necessarily increase measured production. For example, you are a software engineer and your supervisor assigned you a task to complete by the end of the week on Monday. You fire up ChatGPT and complete the task by Tuesday and stop there for the week. You just generated the same output, but with a larger impact on personal welfare. Further efficiency can even suppress GDP growth if firms look to meet demand with fewer inputs (for example, fewer labor hours due to increased productivity, which we are already seeing in the technology market). This illustrates that productivity is rising, but total spending and therefore GDP largely remain constant. This paradox underscores why we have yet to see recent AI breakthroughs reflected in a sharp GDP acceleration.

Further, the measurement system itself plays an influential role. GDP tracks the value of all final goods and services in an economy. This means efficiency-driven price declines can also offset real gains in productivity. For example, let’s say AI agents now schedule all doctors’ appointments. These AI agents are cheaper than schedulers and thus reduce nominal output and result in stagnant growth, even though the economy is more productive.

In sum, AI efficiency seems more likely to boost potential output extremely gradually rather than create near-term growth spikes. As we see adoption broaden and measurement evolve, AI’s contribution could compound, but in the modern AI era, we will likely see a growth similar to prior technological revolutions.

Impact on National Debt

The Trump administration has long championed GDP growth as a method to combat our national debt crisis. A large pillar of the administration’s growth plans revolves around AI efficiency booms. The belief that AI will trigger an immediate boom capable of “outgrowing” our debt burden is dangerously optimistic. While AI can improve efficiency and long-run productivity, the true material effects on GDP are likely to unfold incredibly gradually and unevenly across industries. Historically transformative technologies like electricity and computing took years to diffuse through the economy and start to have real productivity gains. In the near term, much of AI’s impact will center around cost reductions and welfare improvements that GDP accounting does not capture, leaving growth relatively flat. Relying on these delayed gains to offset record deficits and rising interest burdens is fiscally reckless. The Trump administration’s rhetoric assumes AI can generate an exponential increase in output that helps mitigate the debt ratio without making the tough fiscal choices, but the data and history suggest no “boom” is coming.

Conclusion

While artificial intelligence represents a powerful driver of long-term productivity gains, the evidence is hard to refute: its impact on near-term growth will be modest. The notion that AI can ignite immediate and influential productivity booms capable of growing our debt-to-GDP ratio meaningfully misreads economic indicators and historical trends. Gains in total factor productivity will accrue slowly, often masked by welfare gains, a decline in inputs for cost savings, and a slow diffusion across industries. Policymakers who frame AI as a “fiscal silver bullet” risk overestimating short-term growth and structural challenges. The true value of AI comes from expanding potential output gradually over the next decade, something that demands patience, investment, and regulatory autonomy.

You must be logged in to post a comment.