Executive Summary

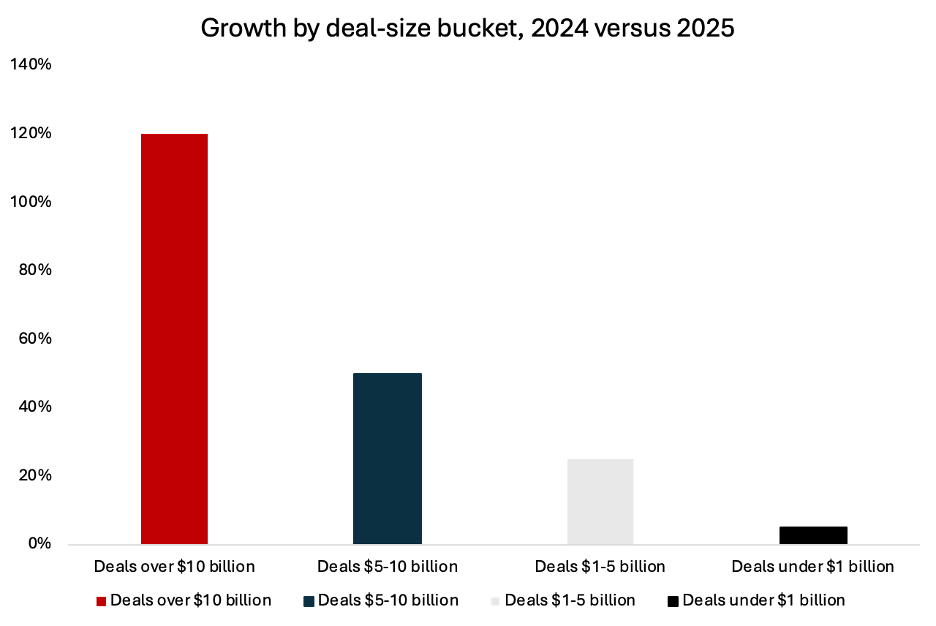

- U.S. M&A transaction value rose roughly 50 percent year over year in 2025, with four mega-mergers above $40 billion versus none in 2024. This happened despite total deal count falling 4 percent. The surge was driven almost entirely by the top of the market: deals over $10 billion grew 120 percent, while those under $1 billion grew just 5 percent.

- Roughly a third of 2025’s hundred largest deals cited AI in their rationale. Falling borrowing costs reopened the deal market, while the strategic race to acquire AI capability drove the mega-deal wave. Notably, Lazard attributes only 20 to 40 percent of the increase to macroeconomic factors, against a roughly 60 percent historical norm, showing how much of the activity was strategic rather than purely cyclical.

- A greater willingness to clear deals with divestitures rather than block them lowered completion risk and aided the recovery. But enforcement only touches the narrow set of deals with significant horizontal overlap, and it never disappeared: the FTC blocked Edwards Lifesciences’ acquisition of Jena Valve in early 2026.

Introduction

Since Donald Trump took office in January 2025, mergers and acquisitions (M&A) activity has spiked. In 2025, total U.S. M&A transaction value increased roughly 50 percent year over year, and the U.S. recorded four mega-mergers valued over $40 billion each in 2025, compared to none in 2024. In 2026, transactions over $100 million rose 65 percent in value year over year.

What has changed? A variety of factors have resulted in a more favorable environment for these transactions. First, while the 2023 merger guidelines remain in effect, antitrust agencies have displayed a greater willingness to clear deals with divestitures rather than block them.

Additionally, interest rates fell, equity markets climbed, private-equity firms sat on record stockpiles of uninvested capital, and the race to scale in AI created urgency to acquire. With several forces moving at once, the key question is which factor best explains the scale of the M&A rebound.

This post argues that improved financing conditions, rising equity values, and the strategic race around artificial intelligence were the main drivers of the rebound, while the shift in antitrust enforcement acted more as an accelerant than the underlying engine.

What are antitrust laws?

Antitrust law was designed to preserve competition by preventing firms from acquiring or abusing market power. Section 7 of the Clayton Act of 1914 prohibits any acquisition whose effect “may be substantially to lessen competition, or to tend to create a monopoly.” That is coupled with the Sherman Act of 1890, which bars monopolization more broadly, and the Federal Trade Commission Act of 1914, which created the agency. These laws set forward a deliberately broad standard, and the use of the word “may” means that the government does not need to prove that harm has occurred or will occur, but that it could occur.

In addition to these laws, the agencies also publish merger guidelines, which lay out how they should analyze deals. Two agencies share enforcement: the Antitrust Division of the Department of Justice and the Federal Trade Commission, which divide deals between them by industry. Under the Hart-Scott-Rodino Act of 1976, companies above a size threshold must notify both agencies before a large merger can close and then observe a waiting period during which regulators decide how to respond. From there, the agencies have several options: clear the deal, issue a “second request” for documents that can delay it by months, block it outright, or settle through a consent decree that permits the deal on the condition that the companies divest overlapping assets. Because the governing standard is broad, much of the real decision-making rests in this discretion: how strictly the same rules are applied.

With the legal framework in mind, the question is not whether antitrust enforcement mattered at all. It did. The better question is whether the shift in enforcement explains the scale of the M&A rebound. The evidence suggests it does not. Financing conditions helped reopen the deal market, AI and strategic scale pressures drove much of the mega-deal activity, and antitrust policy mainly reduced completion risk for a narrower set of transactions.

The Macroeconomic Tailwind: The Cost of Capital

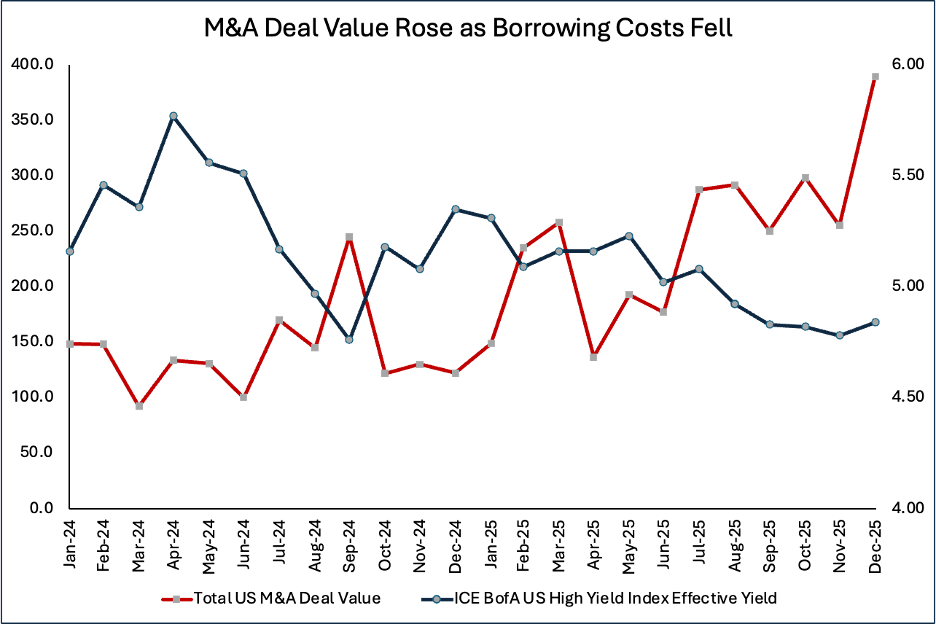

The first major force was the improvement of financing conditions. M&A activity is highly sensitive to the cost of capital because acquisitions are often made with a mix of debt, cash, and equity compensation. When the cost to borrow money falls and equity markets strengthen, deals consequently become easier to finance and easier for boards to justify. Lower yields reduce the cost and risk associated with taking on debt, while higher stock prices give public companies a stronger currency to use as stock-based compensation. In 2025, the cost of borrowing decreased, and the S&P 500 saw another year of solid returns. One way to measure the cost of borrowing is through high-yield corporate bond yields, which measure the borrowing cost for riskier companies, because this is the interest rate that many lower-rated companies must pay to raise debt. The chart below shows the total U.S. M&A deal value in relation to the ICE BofA U.S. High Yield Index Effective Yield, a measure of borrowing costs for lower-rated companies.

However, financing conditions alone do not fully explain the scale or composition of the rebound. Lazard estimates that macroeconomic factors historically explain roughly 60 percent of variation in M&A activity, but in 2025 they accounted for only 20 to 40 percent of the increase. This implies that tailwinds outside of macroeconomic conditions accounted for an unusually large portion of mergers and acquisitions activity. While lower borrowing costs did create the conditions for dealmaking, other forces were needed to make the rise in dealmaking so sharp.

Deal Value Growth Was Driven by Mega-Deals, with the Race to Acquire Scale and Capability in AI Serving as a Key Driver

Looking at growth by deal-size bucket in 2025 compared to 2024, the distribution was notably top-heavy. Deals over $10 billion increased by 120 percent, while deals under $1 billion increased by only five percent. Interestingly, the number of transactions in 2025 fell by four percent, showing how much of the deal value increase was driven by larger transactions.

The clearest explanation for this is that artificial intelligence has created an unprecedented race to acquire scale and capability. As argued by Lazard, the rise of artificial intelligence has widened the gap between winners and losers, which in turn has prompted more urgent and targeted strategic responses. A study by Bain found that 40 percent of megadeals valued at more than $5 billion during the first ten months of 2025 were categorized as transformative, meaning that they represented more than 50 percent of the acquirer’s market cap. In PwC’s analysis of the one hundred largest deals in 2025, approximately one-third cited artificial intelligence as part of the strategic rationale.

It is evident that artificial intelligence was a significant driver of the mega-deals seen in 2025. Research has suggested that anywhere from $5 trillion to $8 trillion could be required over the next five years to fund artificial intelligence technologies and infrastructure. Looking forward, artificial intelligence will continue to reshape business models and is likely to continue driving deal flow as companies compete to scale and acquire these capabilities faster than their peers.

Antitrust: Accelerant, Not Engine

None of this means that enforcement was irrelevant. The shift was significant, and numerous deals cleared that might not have cleared a few years ago. For example, the Justice Department permitted Constellation’s $26.6 billion acquisition of Calpine through a consent decree requiring a $5 billion divestiture and cleared Columbus McKinnon’s acquisition of Kito Crosby on similar divest-the-overlap terms. The willingness to accept structural remedies rather than litigate to block lowered the deal-completion risk that boards price into any large transaction.

However, the magnitude of that channel is inherently limited. Enforcement can only affect deals with horizontal overlap that is significant enough to draw scrutiny, which represents a small share of total deal value. Unlocking that narrow set may have accelerated the recovery, but it cannot account for an across-the-board surge in sectors that didn’t face concentration concerns. Additionally, while the enforcement posture loosened, it did not disappear. In early 2026, the Federal Trade Commission blocked Edwards Lifesciences’ acquisition of Jena Valve.

Weighing the Evidence

Taken together, the evidence suggests that the M&A rebound was not driven by a single factor. Improved financing conditions helped reopen the market and make it easier for acquisitions to be funded. However, those conditions alone do not explain why demand for these transactions grew in the first place. The makeup of the rebound matters. Deal value growth was concentrated in mega-deals, while overall transaction count declined. Many of those transactions were shaped by the strategic race around artificial intelligence, scale, and capability-building.

While enforcement policy has a limited reach, the regulatory environment did contribute to this rebound. A greater willingness to accept divestitures reduced completion risk for some large transactions, which likely gave buyers more confidence to pursue deals that may have faced greater uncertainty in prior years.

In sum, antitrust policy helped clear the path, but it did not create the momentum. Lower borrowing costs made large deals easier to finance, while AI and strategic scale pressures gave companies stronger reasons to pursue them. Antitrust mattered by reducing friction for some transactions, but the engine of the rebound was capital becoming easier to deploy while companies had more urgent reasons to deploy it.

You must be logged in to post a comment.