Executive Summary

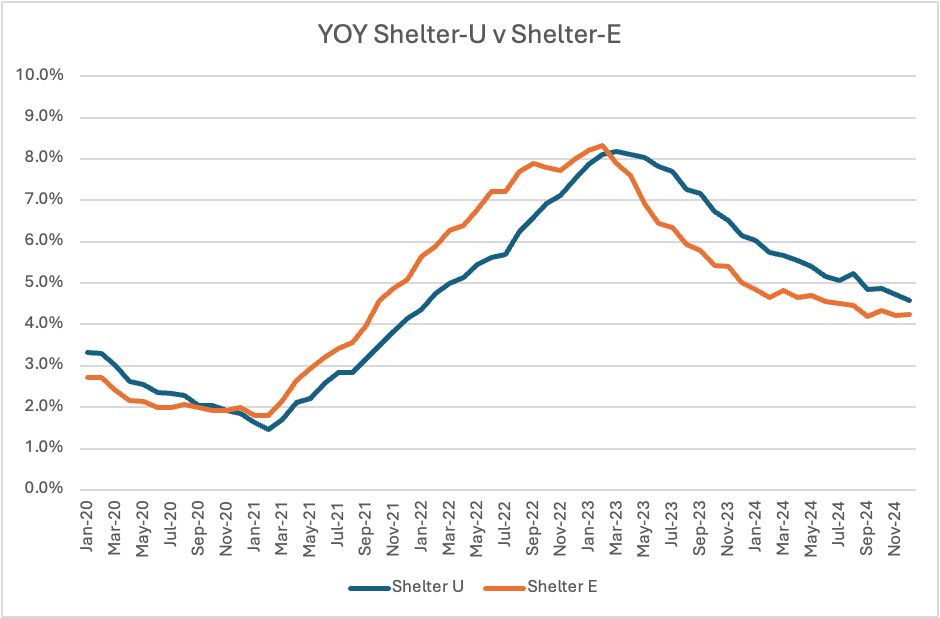

- Recent CPI-U and CPI-E (age 62+) data suggests the elderly have experienced higher CPI growth over the same period, and the heightened rate is likely from a greater weight in the shelter component of CPI which accounts for the housing costs of those who both own and rent their properties.

- Homebuying trends have led to larger houses with more amenities and research suggests homeowners don’t intend on exiting their homes to downsize.

- The boomer generation that bought housing in the late 1990s and early 2000s have been hurt more by the 2020 to 2024 inflationary period, as evidenced by the CPI differences

Introduction

The Consumer Price Index (CPI) is a measure of the change in prices in a typical consumers basket. The elderly tend to consume a different bundle of goods compared to the typical consumer. The Bureau of Labor Statistics (BLS) has introduced an experimental CPI, labeled CPI-E, to determine the relative importance of bundles for seniors. Measuring the change in prices of bundles gives insight to inflationary trends in the most used goods.

Housing occupies a significant portion of income regardless of age, but it is even more apparent for the elderly. The CPI-E reports a shelter weight of 49.5 percent, while the CPI-U reports only 36.7 percent. See the table below for shelter CPI comparisons. Wage growth for this age group has been consistent with CPI growth over this period, aside from the post pandemic recovery where many individuals opted out of work for health reasons. The question becomes why are the elderly spending so much more on housing?

Shifting Generational Trends

Homebuying trends have varied across generations, but those who bought houses in the late 1990s and early 2000s caused the largest changes. Since the 1960s, houses have gotten larger in every category. Average square footage has almost doubled during this period. Boomers are enjoying the hefty increase in size: According to a recent survey by Redfin, 71 percent of 57 to 75 year olds reported wanting to age in their current home. Median home tenure previously was around 15 years, but many people who bought houses at the turn of the century are still in them, 25 years later. Downsizing trends from the past do not apply to this generation. The baby boom generation also owns a higher percentage of 3 plus bedroom houses than other generations. This indicates the emergence of a housing squeeze for younger generations seeking larger houses to start families.

Homebuyers during this period also enjoyed low year over year CPI growth and a favorable housing market. According to the American Housing Survey (AHS) people 55 to 64 reported buying their homes for a median price of $161 thousand, and 65-74 for only $130 thousand. In less than two decades, the new median home price from the BLS is $412 thousand. Homeowners considering moving have certainly appreciated the capital gains increase, but the baby boom generation is staying put.

The Unfortunate Consequences of Homeownership

The capital gains made from home ownership, while significant, are not large enough to warrant moving. People are not downsizing because it is no longer cost effective to do so. Empty nesters are keeping their 3 plus bedroom houses. Holding on to these properties has not come without the associated costs. The mean ratio of the value of housing to household income increases as age increases and has also increased. This ratio could be getting larger because of capital gains on the property, but it is more likely due to lower wages in retirement. The ratio has also increased for all homeowning ages across the board, but the senior population receives the highest. This signifies the exacerbated effect of inflation on the senior population’s ability to own and maintain a home.

The owners equivalent of rent (OER), a subcomponent of shelter in the CPI-E, is not going down. OER is what a homeowner would be paying if they were renting their residence, since home ownership is viewed as a capital investment by CPI standards. So, the increased cost of upkeep of housing is outpacing wage growth for older individuals. Older individuals, by staying in their homes longer, are now reaping the consequences of living in larger homes. They are experiencing the housing crisis along with the rest of the country, but from a different perspective. Because of high inflation and an unfavorable market, people who bought houses at the beginning of the 21st century are essentially frozen in place. A recent survey reported 59 percent of senior homeowners’ main concern is rising maintenance and upkeep costs associated with their current homes. This age cohort is now worse off than the average homeowner today because of the favorable combination of home prices and sizes 20 to 30 years ago.

Recently, there has been a reversal of the trend: House sizes are trending downward again, but their prices are not. Younger generations are buying smaller housing than what they grew up in for the first time in decades. Maybe they are looking at the rising cost of maintaining a larger house, but likely not. Confidence in the ability of young people to afford homeownership is at its lowest level in decades. For the 80 percent of seniors reporting owning homes, affordability is now a concern as well. Somewhere along the way older homeowners became another victim to the housing market.

Conclusion

Homebuying was an accessible milestone in the late 1990s and early 2000s. Today, breaking into the homebuying market is harder than ever. Homeowners are encountering troubles on the other end of the spectrum. Longer tenures in housing are restricting the number of houses available, and those thinking about downsizing have not made enough in capital gains to justify a move. Markets plagued by high inflation have made the costs around owning a house higher than ever before. It seems the senior generation is stuck maintaining a house that is too big for their current household and paying too much to maintain it.

You must be logged in to post a comment.