Executive Summary

- Mercosur and the European Union have signed a sweeping free trade agreement twenty-six years in the making; that same month, Argentina signed its own bilateral trade deal with the United States.

- Despite the optimism surrounding the EU deal, Mercosur is still hamstrung by institutional limitations and diverging member interests, preventing further integration.

- Given this, U.S. trade policymakers are apt to treat Mercosur members as the individual states they are, rather than as the bloc they aspire to be.

Introduction

On January 17th, 2026, Mercosur—a South American customs union comprising Argentina, Bolivia (partial-member), Brazil, Paraguay, and Uruguay—signed a landmark free trade agreement with the European Union. The deal is slated to remove around $4.8 billion in tariffs between the two economic blocs, leading to an estimated 39 percent annual growth in EU exports to Mercosur (from $72 billion in 2024 goods export) and the elimination of EU duties on 92 percent of Mercosur exports. As the product of twenty-six years of negotiations, this deal seems to indicate Mercosur’s viability as a trade and political force.

Yet not a month later, this step toward deeper integration has been partially rebuked by Mercosur’s second-largest economy. On February 5th, Argentine President Javier Milei and President Trump signed their own bilateral trade agreement. Despite the customs unions’ common external tariff (CET), Buenos Aires agreed to remove tariffs on 200+ American products in exchange for Washington eliminating duties on 1,600+ Argentine goods.

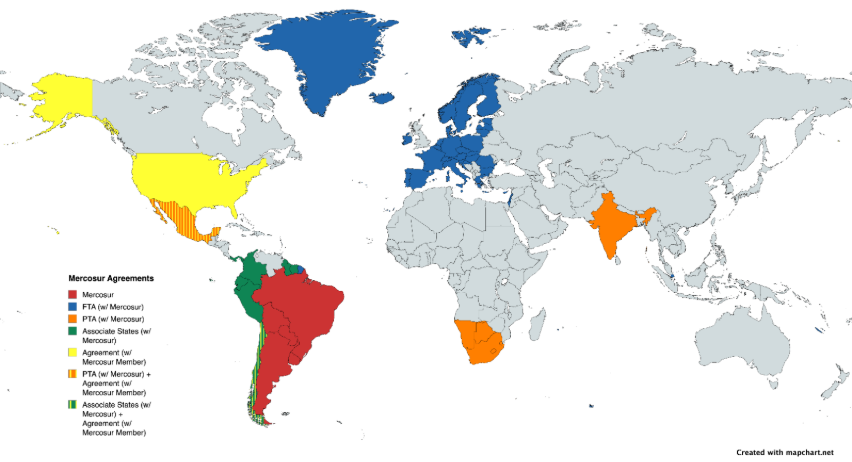

Figure 1: Map of Trade Agreements Involving Tariff Reductions between Mercosur and Third Countries, Mercosur Member States and Third Countries

Source: International Trade Administration; International Trade Administration; Reuters

What this sequence illustrates is the abiding fragility of Mercosur, with the EU agreement as an aberration. This stuntedness, however, was predictable. Mercosur’s institutional frameworks, compounded by the diverging commercial interests of its members, predispose dysfunctionality. Accordingly, American trade policy should continue to approach members bilaterally, as was done with Argentina, rather than as a bloc which does not truly exist.

Why No Integration?

There are two primary reasons why Mercosur has failed to advance further in its goal of economic integration: institutional limitations and inconducive export interests.

Firstly, Mercosur lacks the institutional capacity to operate as a trade bloc. A useful juxtaposition is the 1957 Treaties of Rome, which created the European customs union that would evolve into the common market. The six state signatories agreed to eliminate all intra-bloc tariffs and quotas by 1970, establish an all-encompassing CET, and delegate trade policymaking entirely to the European Commission. The first goal was achieved by 1968, while the latter two stipulations started implementation immediately.

Through maintaining a unified CET without exemptions and then centralizing its administration in a multilateral institution, the inconsistency of Mercosur’s trade policy was avoided in Europe. The Treaty of Asunción allowed members to preserve national trade policies like levying CET-exempt duties. Similarly, Mercosur lacks other typical aspects of a customs union, like a tariff revenue redistribution tool and an updated, universally codified common customs code.

In not managing a total CET, Mercosur fails to pass an early test of economic integration. Enforcing duties—as in a CET—is usually less politically contentious than lowering them; though Mercosur has also not engendered a complete free trade zone, allowing the deterioration of the CET is particularly alarming if the end goal is still an EU-style organization. It attests to the second reason for Mercosur’s floundering integration: conflicting export interests.

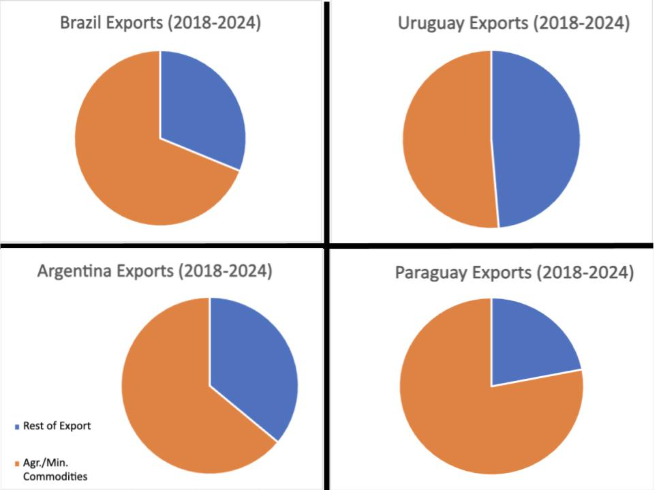

Mercosur exports are predominantly composed of agricultural-, mineral-, and energy-based commodities, limiting intra-bloc trade opportunities. Examining the top five exports by value of Mercosur members in 2024, only Argentina and Uruguay have non-raw materials in the rankings, with beef products, soy products, wheat, gold, petroleum, iron ore, electricity, and other agricultural goods filling the rest of the respective spots. Figure 2 demonstrates how mineral- and agricultural-commodities’ share of exports from 2018-2024 ranges from a high of 78 percent in Paraguay to a low of 50.8 percent in Uruguay (though, if cellulose is included, this rises to 74.1 percent).

Figure 2: Agricultural and Mineral Commodities as Share of Total Exports, Mercosur Members (2018-2024)

Source: OEC Argentina; OEC Paraguay; OEC Brazil; OEC Uruguay

By itself, this reliance on the exportation of similar raw materials restrains opportunities for intra-bloc trade. What invigorates that effect is the presence of a foreign market with extremely high demand. Accordingly, China is Mercosur’s largest export and import partner, with trade flows totaling $180.9 billion in 2025. This was around 4.5x the $47 billion in intra-bloc trade.

While export interests appear to be aligned, without a synchronized trade policy, national governments have pursued their own interests. Paraguay’s continued recognition of Taiwanese independence shuts down a Mercosur FTA with Beijing, which led Uruguay to a failed attempt at a bilateral deal. Meanwhile, many of the tariff exemptions granted to Brazil and Argentina excessively protect fledging manufacturing sectors. Buenos Aires’s backtracking from joining BRICS+ further illustrates alternative foreign policy visions. The Argentina-U.S. agreement is just the latest instance of Mercosur states neglecting coordination for national aims.

Conclusions and Implications for American Trade Policy

The image of Mercosur as a viable player with a definitive interest in global trade is undermined by the institutional and political realities of the bloc. Member states, in their hesitancy to further centralize trade policymaking and prioritization of national interests, have cultivated an organization capable of finalizing FTAs but not of a unified trade policy. Taking this into account, approaching Mercosur as a unit makes unnecessary complications in finalizing desired agreements.

It is possible the EU-Mercosur agreement signals a new phase of reform in the bloc’s troubled history. But until that produces tangible institutional change, the United States should continue the bilateral approach it has applied with Argentina. It is very possible that other Mercosur states are willing to deal in similar disregard of the organization’s constraints if expanded American market access is at stake. Among members, President Luiz Inácio da Silva’s Brazil has been steadfast in its commitment to the bloc. But smaller states, like Uruguay, could be receptive to a bilateral deal; 10% of its exports went to the United States in 2024, and Montevideo has a history of clashing with Mercosur over slow-paced market liberalization. Each member’s unique situation warrants a unique strategy: the EU may overlook this, but the United States has and should not.

You must be logged in to post a comment.