Executive Summary

- One of the United States’ main goals for the 2026 United States-Mexico-Canada Agreement (USMCA) review is to open the supply-managed Canadian dairy market.

- This has been a continuous objective of Washington’s for decades; since 2020, inroads have been achieved, but the scope of such market openings seems unlikely to change in the contemporary geopolitical situation.

- For these reasons, the United States should push for the reform of supply management along the lines of its 2023 dispute with Ottawa, in exchange for partnerships in critical minerals.

Introduction

On December 17th, 2025, United States Trade Representative Jamieson Greer outlined Washington’s objectives for the upcoming 2026 USMCA review before Congress. In what has become a predictable aim of the United States, it was Trade Representative Greer’s main agricultural grievance that drew attention from the Canadian media: the expansion of American dairy’s access to the supply-managed Canadian market.

Canadian dairy supply management has been a thorn in United States-Canada trade relations since its institutionalization in 1971. The system, which combines several economic measures to foster a protected, producer-catered Canadian dairy market, involves tariff-rate-quotas (TRQs) preventing excessive imports of foreign dairy. Geographically close American farmers are the primary losers from the apparatus, given the perishability of the products involved.

Trade Representative Greer’s comments echoed an enduring dissatisfaction expressed by President Trump. Reducing dairy TRQ barriers was one of the USMCA’s achievements during the first Trump Administration, while in June 2025, the President took to Truth Social to decry Canada’s steep tariffs (north of 200 percent) that kick in once the non-tariffed import quota is met. Ottawa has proven both willing to compromise in expanding the non-tariffed TRQ, but resilient in never dismantling the immensely popular policy.

With Canada’s substantial commercial reliance on the United States, the 2026 USMCA review is a tempting chance to aggressively push for larger market openings if not the end of supply management. Ultimately, however, the latter outcome is neither feasible nor the most beneficial for either country. Rather, American negotiators should push for reforms to the system along the lines of the 2023 USMCA dairy dispute, offering collaboration on strategic investment in exchange.

A Brief History of Supply Management

The system of supply management was formalized by Ottawa in 1971 amid concerns over unsustainably low dairy prices, but a lack of government funds to engage in the subsidization employed south of the border. Accordingly, a three-pillared arrangement was legislated to keep dairy prices artificially high in the domestic market. Exports were largely foregone in exchange for consistent returns from Canadian farmers selling to Canadian consumers.

The three pillars are as follows. Price mechanisms guarantee farmers a minimum price for their dairy products. To make the market operate with this price, controlled production is established, where farmers are allocated a quota of dairy production from provincial marketing boards. Lastly, and most poignantly for trade, import controls in the form of TRQs are in place to hedge against cheap foreign dairy desynchronizing the managed price.

In its 50+ years of operation, Ottawa has achieved its coveted smaller-farm, higher-price equilibrium. In 2024, the average Canadian dairy farm had 105 cows compared to the average American farm’s 283 cows (2021). In 2025, the average gallon of Canadian milk ran consumers around $0.89 more than the average American gallon ($4.96 vs. $4.07). Although smaller Canadian dairies turn a profit, between 2000 and 2017, that price distortion cost Canadian consumers an additional $2.7 billion.

The Weakest Link: TRQs

Despite billions in added consumer prices, Ottawa has historically been reticent to reform supply management. In painstaking negotiations, the United States-Canada Free Trade Agreement and the North American Free Trade Agreement both concluded with exclusions for Canadian dairy liberalization. While harsher quantitative restrictions on dairy imports were replaced with TRQs in 1995, pre-2018 import restrictions were vehemently upheld in the face of American legal challenges and attempted circumventions.

This all changed in 2020 with the entry-into-force of the USMCA. The First Trump Administration wrangled the highest-ever non-tariffed TRQ amounts, a plan for annual increase in that allowance through 2039, and the elimination of class 7, a Canadian milk designation which American producers had long alleged hurt imports. With this recent susceptibility to barrier reduction, stubborn food price inflation, and the extra costs supply management inflicts on consumers, in 2026, Ottawa appears prone to abandoning its status quo protectionism.

The Politics of Supply Management

Integrally, this ignores the political salience of the apparatus. Supply management has been pitched to the Canadian public as a means of asserting economic independence from the United States. This broad support (around 69 percent of citizens), supercharged by the contemporary low point in United States-Canada relations, makes for a climate where American market concessions are more likely to result in electoral losses for the ruling Liberal Party.

When juxtaposed to where Canadian dairy producers and processors are concentrated, this factor becomes even more pressing. The 2024/2025 total milk quota distribution saw 36.7 percent of production distributed to Quebec, and 31.9 percent to Ontario, Canada’s second and first largest provinces by population respectively. Primarily, these producers cluster in Quebec and southern Ontario, characterized by fickle ridings that either voted conservative, were swayed by the Bloc Québécois, or went Liberal by small margins in the 2025 Canadian election. Placating dairy farmers, therefore, is vital to maintaining Prime Minister Carney’s government.

Consequently, Prime Minister Carney has doubled down on supply management every chance available, most recently in December 2025. The Bloc Québécois has latched onto the issue, spearheading Bill C-202 in June 2025, which prevents the Canadian foreign minister—but not the PM—from offering increases in TRQ allowances or lessening the over-quota tariff. With a pro-farmer alternative readily available, the electoral toll from destabilizing supply management would be heavy.

USMCA Disputes

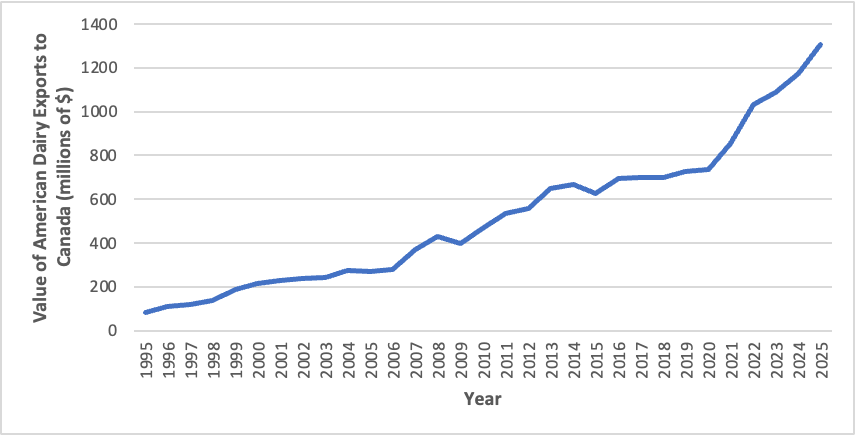

That said, since the 2020 USMCA TRQ reforms took effect, American dairy exports to Canada have grown precipitously. From 2010 to 2021, exports increased by 48 percent, going from $466 million to $692 million. As of 2024, American dairy exports to Canada alone were worth $1.14 billion, while global Canadian dairy exports hit only $554.7 million total.

Figure 1: Growth of American Dairy Exports to Canada, 1995-2025

Source: USDA FAS

Yet, this market opening has not been without contention. Two USMCA panels have been assembled—one in 2021, one in 2023—to rule on disputes on the implementation of TRQ reductions. In 2021, language in the milk, cream, and butter TRQ categories reserved 85-100 percent of these import allowances to Canadian processors. This led to mostly low-value American dairy (ex. large blocks of industrial cheese) filling it up, harming American producers farther down the value-added chain. A 2022 ruling found merit in the American grievances, with Ottawa striking the processor reservation and shifting TRQ allocation to be based on historical market activity.

The 2023 dispute resolution was less to Washington’s favor. Taking additional issues with the TRQ allowance process, the claim centered on the ineligibility of non-distributors or processors from applying for a share of the non-tariffed import quota. This chiefly affects American retailers like Walmart and Kroger, whose inclusion would bring American imports far closer to the TRQ ceiling; retailers sold $76 billion in dairy to Americans in 2023. Coupled with the eligibility complaint was discontent over the phrasing Canada used when asking American producers their desired TRQ allowance, alleged bias toward processors in the TRQ consideration process, and slow redistribution of unused or returned TRQs. Unlike in 2021, the panel sided with Ottawa, finding all Canadian actions technically in compliance with the 2022 decision.

Compromise: 2023 Claims for Investment

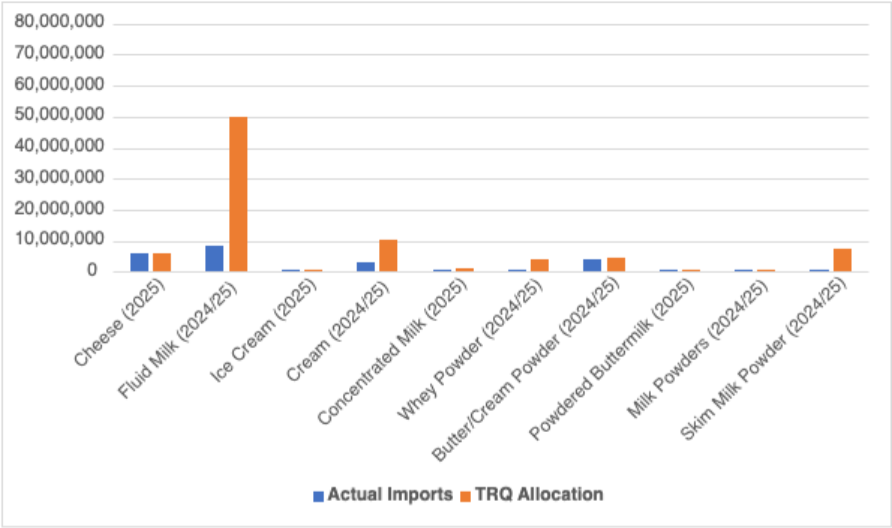

No matter the rapid rise of dairy exports to Canada, the room for continued American export expansion is striking. Looking at ten of the fourteen TRQ categories, figure two displays how only two—cheese and ice cream—more than halfway filled their no-tariff allocation in 2025. Producers assert this is largely due to the discriminatory allocation of the TRQ, and certain firms, like retailers, being unable to participate.

Figure 2: Fulfillment of USMCA Dairy TRQs (kgs), 2025-2026

Source: Government of Canada

Under the guise of making good on the original USMCA reforms while both needing a politically tolerable development for their domestic dairy industries, Ottawa and Washington could apply the American-advocated 2023 changes in the 2026 review. This would not force Canada to ostensibly expose its farmers more than in 2020, let the Second Trump Administration pose as rectifying a disadvantaged trading situation, and potentially bring slightly lower prices to North American dairy consumers.

Still, Canadian negotiators could balk at any maneuvering to unrig supply management. Its political weight is unlike most other economic initiatives. To solidify the deal and follow both governments’ stated policy objectives, the 2026 USMCA review could add an investment component into Canadian critical minerals and infrastructure. A hallmark of Prime Minister Carney’s government has been the Major Projects Office, financing improvements across Canada, including natural gas pipelines, mines, and nuclear plants. This, coupled with Canada’s abundance of strategic resources, makes it the ideal investment environment for Washington’s global critical minerals campaign. A partnership could take the form of several major projects being announced with American financing, full Canadian membership in Pax Silica, or an agreement to prioritize the funneling of Canadian uranium to American nuclear reactors.

Conclusions and Policy Implications

The 2026 USMCA review is shaping up to be a contentious focal point for United States-Canada relations, with dairy supply management at the center. By accounting for the factors weighing on both sides’ negotiating posture, a comprehensive, politically justifiable outcome like the TRQ reform for critical investment proposal can be reached. Fundamentally, these countries have shared interests in developing North American resources and strengthening their integrated market. Since 2025, this has primarily been prevented by the politics of Canadian nationalism and raucous American rhetoric. In the USMCA review, there is an opportunity to bring the relationship into alignment: to miss it would mean two more years of harmful decoupling.

You must be logged in to post a comment.