Executive Summary

- President Trump aims to rebalance global trade by imposing tariffs and welcoming a weaker dollar because he views the U.S.’ large trade deficit as evidence of unfair trade practices.

- However, shrinking the trade deficit will shrink the capital account surplus that balances it, thereby weakening the dollar as foreign investors move away from U.S. assets.

- Less foreign investment may weaken the dollar, raise federal borrowing costs and slow the creation of high-paying jobs.

Introduction

President Trump has long called for the U.S. to impose higher tariffs to reduce the trade deficit, which he has declared a national emergency. His administration announced unprecedented unilateral tariffs to reverse what it alleges are unfair trade practices. This strategy ignores the accounting principle known as the balance of payments: The country’s current and capital accounts must balance, meaning that reducing the trade deficit will also reduce the capital account surplus. This rebalancing has prompted a global “sell America” trend. Foreign investors hold a significant portion of U.S. Treasuries and equities, helping finance the national debt and promote growth of U.S. companies. A drop in foreign investment may strain the federal budget by raising borrowing costs.

Balance of Payments

President Trump has built his trade agenda around the central belief that trade deficits prove other countries are “ripping off” the United States. This logic ignores the balance of payments accounting identity, which measures the financial transactions between U.S. residents and the rest of the world. The United States runs a current account deficit, which is balanced by a surplus in its capital and financial accounts. The current account, which primarily consists of the trade deficit, measures the net flow of goods, services, and one-way transfers such as foreign aid or remittances. The capital and financial accounts in the U.S. represent a net inflow of foreign capital in the form of foreign direct investment and portfolio investment.

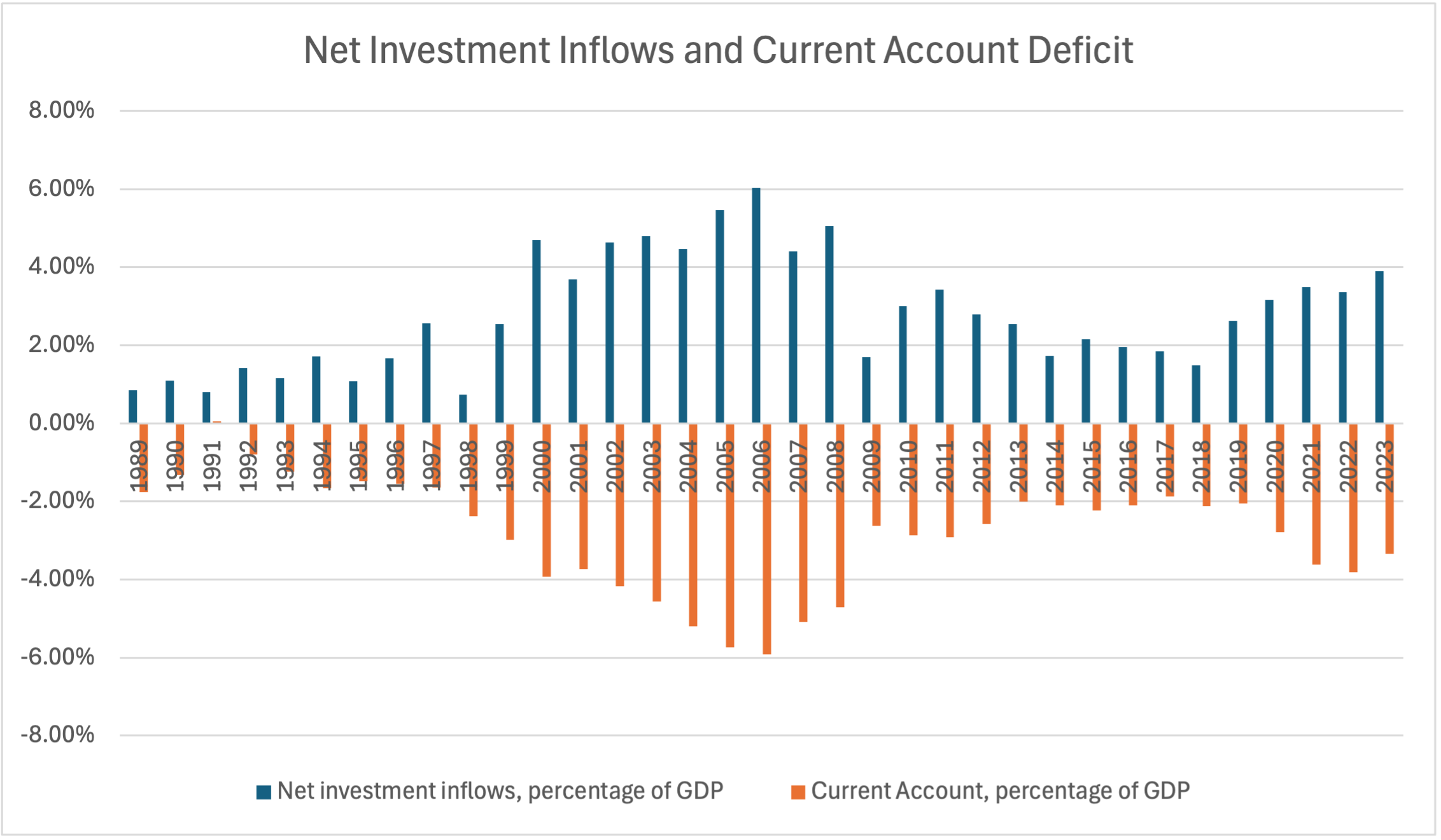

Because the accounts must balance, a reduction in the current account deficit would shrink the capital account surplus. This balancing act occurs in part because when the US imports goods, the exporting countries then hold U.S. dollars. Those countries typically reinvest those dollars into U.S. securities such as Treasuries because they are highly liquid, offer interest rate returns, and are viewed as a safe haven investment. Some countries also hope to depress their currency against the dollar, making their exports more attractive. Figure 1 shows that from 1989–2023, the data show a strong negative correlation between net investment inflows and the current account deficit.

Figure 1:

The U.S. attracts high levels of foreign investment, due to its high market liquidity, deep supply of investment opportunities, strong corporate governance, and mature market infrastructure. This drives up the value of the dollar, because U.S. assets must be paid for with U.S. dollars. When the dollar is strong, exports are more expensive relative to those from other countries, while imports are cheaper. This is in large part why the United States runs a large trade deficit with the rest of the world. The balance of payments explains that this trade deficit is necessary for the United States to continue receiving such high levels of foreign investment.

Impacts of Shrinking Capital Account Surplus

A lack of American savings and domestic investment partially fuels this reliance on foreign money. Since 2018, the United States has by far been the largest recipient of foreign direct investment and has consistently been a popular destination for passive investment. At the end of June 2024, the U.S. Treasury Department reported that foreign investors owned 21 percent of all U.S. securities, valued at $30.9 trillion. Broken down by investment type, foreign investors owned 33 percent of U.S. Treasuries, 27 percent of U.S. corporate debt, and 18 percent of U.S. equities outstanding. In contrast, the Treasury found that U.S. investors held only $15.3 trillion of foreign securities at the end of 2023, mostly in the form of long-term debt issued by private corporations.

With foreign investors holding a third of Treasury bonds, a decline in foreign demand would increase borrowing costs for the federal government, making it more difficult to roll over federal debt. The 30-year Treasury has hovered near 5 percent since May, following Moody’s downgrading of the United States’ triple-A credit rating. Concerns around the fiscal deficit are growing, especially as the Congressional Budget Office estimates that the recently passed budget reconciliation bill will increase the deficit by around $4 trillion over the next decade.

Foreign direct investment also crucially generates high-paying jobs, as Bureau of Economic Analysis data show that FDI from multinationals created nearly 8.4 million jobs in 2022, offering an average annual compensation of $89,296. These companies also paid 19 percent of all federal corporate income taxes, representing a significant source of revenue for the federal government.

Conclusion

Contrary to President Trump’s convictions, reversing bilateral trade deficits will not save the U.S. economy and domestic employment. The administration’s efforts to reduce the trade deficit will shrink the capital account surplus that balances it, as trade and geopolitical uncertainty drives foreign investors away from U.S. assets. Declining foreign investment will devalue the dollar, increase borrowing costs for the federal government, and reduce the number of high-paying jobs generated by FDI.

You must be logged in to post a comment.