Executive Summary

- Throughout 2025 and 2026, China has leveraged its control over critical mineral supply chains, forcing the United States to the negotiating table; the resulting shortages caused disruptions in the production of goods from automobiles to computers.

- In February 2026, the Trump Administration inaugurated Project Vault, a critical minerals stockpiling program intended to reduce exposure to foreign-induced supply shocks through storing minerals for civilian use.

- Although Project Vault is a step in the right direction, addressing concerns over critical mineral supply chains warrants a holistic approach, including codified legislation and de-risking incentives.

Introduction

On April 4th, 2025, China imposed export controls on seven rare earth minerals and associated magnets in response to tariff increases by the United States. In the month these measures were formally in effect, American automakers, defense contractors, and technology firms experienced logistical delays, forced to scale back or even halt production at plants across North America. At the urging of hurt industries, the Trump Administration initiated negotiations in May, culminating in a 90-day tariff truce with Beijing in exchange for the lifting of controls.

Five months later, as trade tensions flared again, China passed a set of modifications to its 2020 Export Control Law. Under the revised legislation, the list of export-controlled “dual-use” goods and technologies was expanded, notably including critical minerals like tungsten, gallium, antimony, and medium-to-heavy rare earths. Like in May, a meeting was rapidly arranged between President Trump and President Xi Jinping. Once more, China lifted its controls for further American tariff concessions.

As evidenced by these two incidents, China dominates the critical mineral supply chain. In 2024, 99 percent of global rare earth mineral processing capacity was based in the country. This monopoly, coupled with large productions of other vital minerals like graphite, has been wielded by Beijing as a tool of foreign policy coercion. Before the United States suffered such treatment, Japan had been subjected to even harsher export controls in 2010 and would be the target of another set of politically motivated export restrictions in 2026.

In the absence of dependable critical minerals sourcing, countries have increasingly embraced the practice of stockpiling. The American iteration, Project Vault, combines public-private consultations with market-based purchases of minerals to guarantee low-priced resources for participating firms during a shortage. It is one prong of the Trump Administration’s multi-faceted goal: secure a reliable mineral supply chain.

Though Project Vault somewhat rectifies exposed American minerals logistics, it is missing crucial components present in comparable policies abroad. To maximize its utility, longevity, and efficiency, the United States must reform Project Vault through legislative codification, incentives for domestic sourcing, and the promotion of both mineral recycling and substitution.

What are Critical Minerals?

The United States Geological Survey defines critical minerals as minerals vital to American economic or national security. As of 2025, resources like zinc, chromium, copper, yttrium, vanadium, and 55 others were designated as such by the USGS. Minerals’ criticality evolves with their industrial uses. Contemporary critical minerals are integral to producing goods like computers, automobiles, defense technologies, and cell phones. Of USGS’s 60 listed minerals, 17 are further specified as rare earths, or materials that are especially difficult to extract.

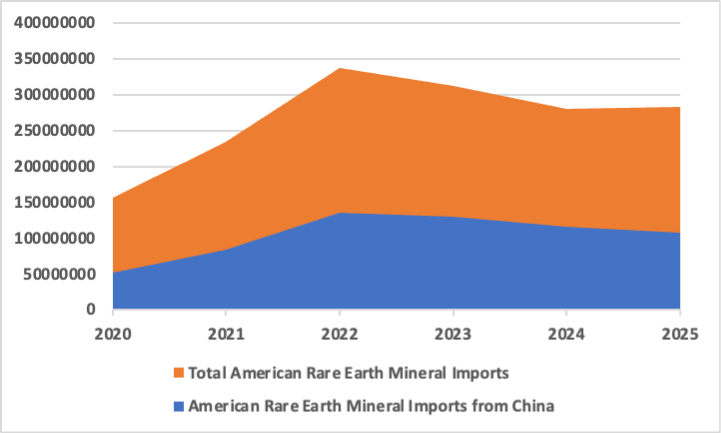

China has long pursued a policy of cornering the critical minerals market through state-backed investment and coordination. As of 2024, 59 percent of international rare earths production and 91 percent of rare earth refining capacity were in China, while Beijing represents 60-99 percent of global mining/refining of many critical minerals like gallium (99 percent), tungsten (83 percent), titanium (69 percent), and antimony (60 percent). The properties of these minerals are often not replicable, making substitution infeasible. American imports of critical minerals from China vary by material but are highest as a share of total imports for rare earths.

Figure 1: Chinese Imports as Share of Total American Rare Earth Imports (Millions of $); 2020-2025

Source: United States International Trade Commission

American Mineral Stockpiling

The United States has been stockpiling minerals for defense purposes since the Strategic and Critical Minerals Stockpiling Act of 1939, but Project Vault is the first to store minerals for civilian use. Its coinciding executive order outlined a structure built on private-sector cooperation and market-based sourcing.

Using a $10 billion loan from the Export-Import Bank of the United States and another $2 billion in private capital, Project Vault stocks minerals based on demand. Producers first purchase space in the reserve and submit a request for certain minerals to be stored. Then, they set a forward price to re-access those minerals, paying upkeep and storage fees until they tap the stockpile amidst supply disruptions. Firms gain from hedging against future high prices, while the government is assured of a controlled economic fallout if Beijing institutes export controls. Ideally, Project Vault will store 60 days’ worth of minerals.

Corporations like GE Vernova, Boeing, and Clairios have expressed interest in Project Vault. Though one of its goals is to stoke domestic critical mineral production, it is not clear if domestic sourcing is incentivized or in what form (ore, by-product, processed good, etc.) minerals will be stored. In maximizing the benefit of Project Vault, domestic suppliers need priority, while partner firms require access to industrially useful mineral products.

Stockpiling Done Right: Japan

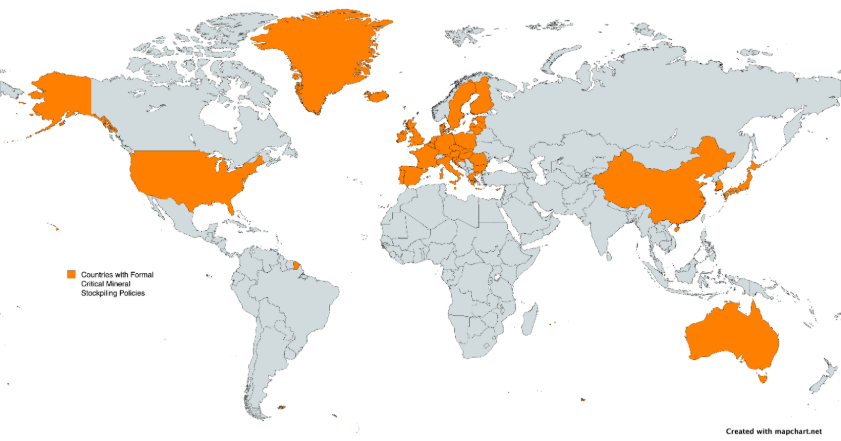

Figure 1: Countries with Formal Critical Minerals Stockpiles

Sources: International Energy Agency, Bloomberg, Reuters, European Commission

Outside the more recent threat of Chinese export controls, the importance of critical minerals has incentivized governments to begin mineral stockpiles. In the event of a logistical failure, conflict, or other disruption, stockpiles can be a brief respite for the private sector to avoid hiking prices.

Of the many countries that have instituted stockpiling strategies, Japan stands out for its comprehensive approach of technological innovation and curating reliable sources. Japan initiated its stockpile program in 1983, and in 2002, major reforms led to the formation of Japan Oil, Gas, and Metals National Corporation (JOGMEC) from two prior agencies. JOGMEC is responsible for both the stockpile and exploitation of critical mineral resources in Japan.

Subsequently, when China imposed a critical mineral embargo against Tokyo over a border dispute in 2010, Tokyo launched a vigorous derisking campaign away from Beijing. To realize that reduced trade, JOGMEC directed exploration of marine mineral deposits, promoted methods to reduce total mineral usage (ex. concentrating dysprosium on magnet surfaces), invested in mines and facilities in friendly countries, and received increased funding for mineral exploitation schemes. Tokyo also incentivized scaling urban mining operations, a uniquely Japanese industry of mineral recycling from citizen waste.

Though critical mineral-using firms in Japan are still enmeshed with Chinese mineral refiners and processors, the efforts of the last decade and a half have paid off. In one of JOGMEC’s most successful projects, the exploration of muds on Minami-Tori-Shima Island yielded a 16-million-ton rare earths deposit containing 15 minerals. Concurrently, as of 2025, 10 percent plus of global tin, tantalum, and indium reserves originate from Japanese urban mining, despite the country having sparse natural deposits. Overall, China’s share of total Japanese critical minerals imports fell from 85 percent in 2010 to 63 percent in 2024, representing significant progress largely from decisive government action.

Revitalizing Project Vault

Like Japan’s programs, three reforms can ensure Project Vault is an effective policy to build safe critical mineral access and cater the stockpile to only those most inaccessible materials.

First, Project Vault needs to be enshrined in legislation. This program should be firmly established with a statute as opposed to its contemporary, executive order-derived existence. In doing so, future presidents will not have the discretion to abandon Project Vault, while the prospective codified policy can be expanded with the same guarantee of continuity. It must also specify what form of critical minerals will be stored. The United States lacks significant processing capacity, so stockpiling raw ores would be of no value to manufacturers compared to derived products like magnets and powders.

In outfitting a Project Vault bill, three new aspects need to be added: support for domestic or allied mineral sourcing, tax credits for critical mineral recycling or use reduction, and an urban mining technician exchange program with Japan.

The former may take the form of a minimum share of the stockpile having to be from American or allied mines to the extent that this is possible. This would stoke demand for increasing production of domestic critical minerals while maximizing dependable sourcing of minerals that do not have to be imported.

The second recommendation reckons with the slow scaling of certain supply chain steps like mineral refining. As the United States builds out its capacities in those sectors, minimizing the use of critical minerals is a simple way for stakeholders to lessen the ramifications of foreign export controls in the interim.

The recycling tax credit and exchange program will aim to bring the Japanese practice of urban mining to the United States. Tokyo has already engaged in research partnerships with countries like Indonesia and the Philippines to export the practice. With Washington’s goal of reshoring industry and critical minerals production, the jobs and strategic resources that would be gained from an American version of the Japanese enterprise are attractive pretexts.

Conclusions and Implications

The geopolitics of critical minerals have already been shown to be a potent force in trade disputes. As China increasingly uses export controls to achieve strategic objectives, stockpiling the vital resource provides a guarantee against immediate economic instability for the United States. Furthermore, making Project Vault a long-term project gives American producers of automobiles, electronics, etc., certainty to continue expanding their production. Learning from the example of Japan, a congressionally backed Project Vault should then be built out to encompass domestic production incentivization and efficiency. Taking a multi-faceted approach to critical minerals security is the most effective means of remedying an unfavorable status quo.

You must be logged in to post a comment.